The reforms that have been promoted in the banking sector by the National Bank of Moldova aim to assure the development of a healthy corporate governance and in compliance with the international principles, as well as to keep a strong, safe and transparent banking sector based on market principles.

As of 30 September 2018, 11 banks licensed by the National Bank of Moldova operated in the Republic of Moldova. Following the qualitative changes in the structure of shareholders in the banking sector, currently, more than 70 percent of the bank assets are operated by international groups with solid reputation. By comparison, in 2016, slightly more than 20 percent of assets were operated by international groups.

Hence, new strategic shareholders have entered the banking sector of Moldova:

-

Banca Transilvania of Romania, with the support of the European Bank for Reconstruction and Development (EBRD), became an indirect shareholder of the C.B. "VICTORIABANK" S.A.;

-

Intesa Sanpaolo from Italy – a sole shareholder of the C.B. "EXIMBANK" S.A, the latter becoming part of the Intesa Sanpaolo Group;

-

In addition, in October, the single block of shares of 41.09 percent of the C.B: „MOLDOVA-AGROINDBANK” S.A. has been purchased by a consortium of investors consisting of EBRD, Invalda INVL and Horizon Capital.

Also, starting with 30 July 2018, banks have submitted the first COREP reports in accordance with the BASEL III requirements. The rate of own funds recorded 28.8 percent, within the limits forecasted by the NBM, and above the minimum of 10 percent and the combined buffers. According to the new reporting framework, the requirements towards the own funds have been calculated under the new methodology, by considering not only the credit risk, but also the market and operational risk. Concomitantly, for purposes of prevention and attenuation of the macro prudential risk or the systemic risk, additional requirements for own funds have been established, which the banks must comply with, in order to constitute capital buffers.

In addition, in the first 9 months of 2018, the tendency to consolidate own funds (previously TRC-total regulatory capital) in the banking system has continued, by keeping a high level of liquidity and profitability. Furthermore, the assets and deposits continued to increase. Compared to the end of the previous year, the loan portfolio has increased in the banking sector. Therefore, the loan portfolio has been increasing monthly since March 2018. The share of non-performing loans in the loan portfolio has diminished, but still records high values.

Steps taken by the National Bank of Moldova with regard to the three largest banks in Moldova

On the 22 August 2018, by decision of the Executive Board of the National Bank of Moldova (NBM), the intensive supervision measures against the C.B. „VICTORIABANK” S.A. have been lifted, following the ensuring of transparency by the bank, regarding the structure of bank’s shareholders. At the same time, the new Council of administration of the bank has been approved and became operational as of 9 August 2018.

Currently, the C.B. „MOLDOVA-AGROINDBANK” S.A. is under intensive supervision (from 2015), while the C.B. „Moldindconbank” S.A. – under early intervention regime (from 2016).

Therefore, on 30.09.2018, the C.B. „MOLDOVA-AGROINDBANK” S.A. and C.B. „Moldindconbank” S.A., jointly hold 47.5 percent of total banking sector assets.

At the same time, to prevent the banks from being exposed to excessive risks, the activity of the banks to which the intensive supervision and early intervention measures were applied has been daily monitored by the National Bank. Given the above, the financial situation of these banks, their transactions, the agenda of the management bodies’ meetings, etc., are being constantly reviewed.

At the same time, by decisions of the Executive Board of the National Bank of 26 April 2018, some entities have been qualified as related parties of the C.B. „MOLDOVA – AGROINDBANK” S.A. and the C.B. ,,Moldindconbank” S.A., as a result, the prudential limits associated with the related parties have been exceeded. The above mentioned banks submitted to the NBM their remedial action plans on the steps to be taken to ensure their compliance with the prudential limits set for exposures to related parties as well as the improvement of their internal control systems for the identification and monitoring of related parties, which were examined and approved by the NBM. Therefore, the banks submit reports to the National Bank of Moldova on the undertaken measures on a quarterly basis.

C.B. „MOLDOVA – AGROINDBANK” S.A.

During the process of monitoring the transparency of banks’ shareholders, the National Bank of Moldova has identified two groups of shareholders of the C.B. „MOLDOVA-AGROINDBANK” S.A., who have acted in concert and purchased a substantial quota in the share capital of the bank amounting 43.1 percent, without the prior written approval of the National Bank. Therefore, the above-mentioned shares were to be disposed of within a three-month period. As the shares had not been disposed of within the set time limit, they were cancelled by the bank, the new stock being issued instead. Thus, the above-mentioned shares were put up for sale, but they were not sold within the set time limit. Subsequently, the sales period was extended several times. On 19 June 2018, the NBM Executive Board granted to an international consortium of investors (EBRD, Invalda INVL and Horizon Capital) its prior approval for the acquisition of the 41.09 percent of the bank's share capital. As a result, in July 2018, the Public Property Agency bought the above mentioned stock which had to be put up for sale within three months on the regulated market as a single block of shares, by open outcry auction. On 2 October 2018, the single block of shares of the C.B. „MOLDOVA-AGROINDBANK” S.A. has been sold at auction to the international consortium of investors (BERD, Invalda INVL and Horizon Capital).

In addition, on 22 November 2018, the General Meeting of Shareholders will take place, to be examined the new composition of the bank’s council.

C.B. „Moldindconbank” S.A.

Following the finding out by the NBM that a group of persons had acquired and became a holder of a qualifying holding of 63.89 percent in the bank's share capital, with no prior written approval from the NBM for this acquisition, on 20.10.2016, the NBM applied the early intervention regime against the C.B. „Moldindconbank” S.A., which is currently maintained.

The above- mentioned block of shares have not been disposed of in the time limit set by legislation, hence, in January 2018, they have been cancelled. The bank issued a new stock accounting for 63.89 percent of the bank's share capital, and put it on sale for a three-month period as a single block of shares at an initial selling price, which was set by an international audit company. The term for sale has been extended for three months by decision of the NBM Executive Board of 11 July 2018, but because the shares have not been sold in the set time limit, on the 12 October 2018, the term has been extended until January 2019. Under the Law on the Banking activity no 202 of 06.10.2017, the National Bank can dispose the extension of the three-month term no more than three consecutive times.

In addition, on 19 October 2018, the NBM Executive Board decided to extend the mandates of the bank’s interim administrators of the C.B. „Moldindconbank” S.A. for a six-month term, until 20 April 2019.

Currently, the above-mentioned banks follow their normal operating routines providing full range of services, including those related to deposits, lending and settlement operations.

Steps taken by the National Bank of Moldova with regard to other banks

In the analyzed period, the NBM Executive Board has applied sanctions against several banks, as well as to several shareholders.

Following the assessment conducted by the central bank, the NBM’s Executive Board, at its meeting held on March 21, 2018, decided to apply sanctions on the direct holder of a qualifying holding of 4.92% in the share capital of C.B. ”ENERGBANK” S.A. for its non-compliance with the requirements regarding a shareholder’s suitability and financial soundness, stipulated in art. 48 of the Law no. 202 of 06.10.2017 on the Banking activity. In addition, NBM decided to sanction two shareholders of „Banca de Finanțe și Comerț" S.A. with a fine in amount of MDL 179.5 thousand, for failure to provide the information requested by the NBM for the assessment of the quality of the shareholders.

At the same time, fines have been applied to two other banks, following the full-scope inspection. Respectively, the National Bank of Moldova Executive Board decided to impose a fine against “Banca de Finanţe şi Comerţ" S.A. in the amount of MDL 362.1 thousand and a warning against the members of the Bank's Board, following the on-site full-scope inspections carried out at this bank, where violations of the Law on Financial Institutions, the normative acts of the NBM and the Law on the prevention and combating of money laundering and terrorist financing have been identified.

In addition, the NBM decided to apply a fine on the C.B. "COMERTBANK" S.A. and the members of its Board in a total amount of MDL 2.25 million, and a warning on the members of the Board. Another warning has been imposed on C.B. „EuroCreditBank” S.A.

Following the verification of transactions with the bank’s related parties within the previous off-site inspections of the bank, under the new amended legislation, in July 2018, the National Bank decided to qualify several persons as related parties to four banks and requested those banks to develop and submit their remedial action plans listing measures to be applied that would improve their related parties identification and monitoring processes, while for two banks out of the four, plans of compliance of exposures towards the related parties with the prudential limits have been requested. The banks submit quarterly reports on the undertaken measures and their results.

Financial situation of the banking sector and the compliance with prudential regulations

As of 30 September 2018, based on the report data submitted by licensed banks, the situation in the banking sector was characterized by the following trends:

Assets and liabilities

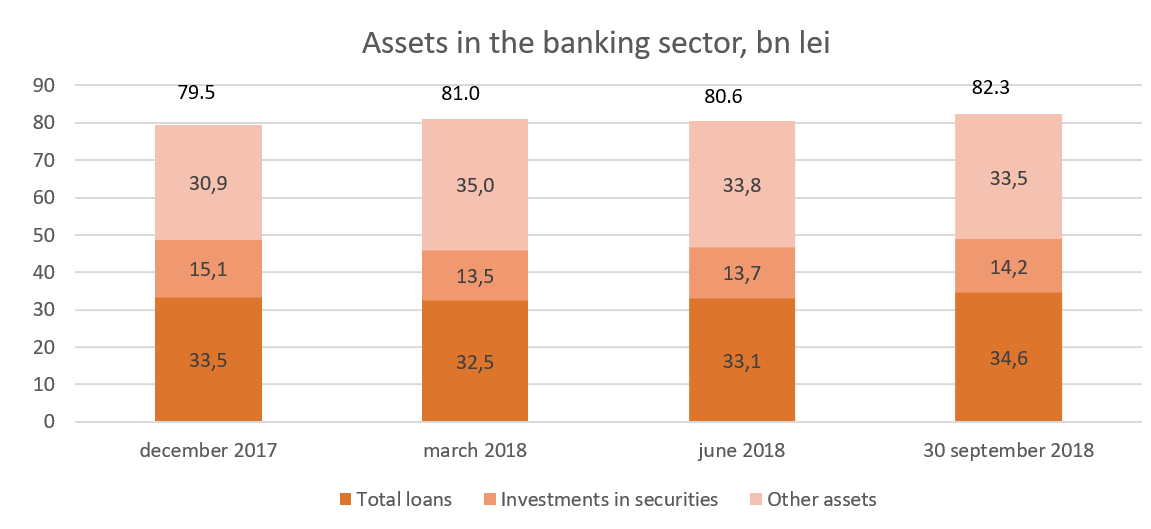

Total assets recorded MDL 82.3 billion, increasing by 3.6% (MDL 2.8 billion) during the first nine months of 2018.

As of 30.09.2018, the balance of the gross loan portfolio accounted for 42.0% of total assets or MDL 34.6 billion, having increased by 3.3% (MDL 1.1 billion) during the reference period. At the same time, the volume of new loans increased by 14.9% during the first nine months of 2018 compared to the same period of the last year. One of the factors that led to this growth is the decrease of the interest rate on loans during the nine months of 2018.

In addition, starting from March 2018, a monthly increase in the loan portfolio is being recorded, despite the fact that non-banking organizations have intensified their lending activity. The largest growth in the last nine months of 2018 has been recorded in the consumer and real estate loans.

Investments in securities (certificates of the National Bank of Moldova and government securities) accounted for 17.3% of total assets, having decreased by 1.7 pp. compared to the end of 2017.

Other assets accounting for 40.7% are kept by banks in accounts opened with the National Bank of Moldova, with other banks, in cash, etc.

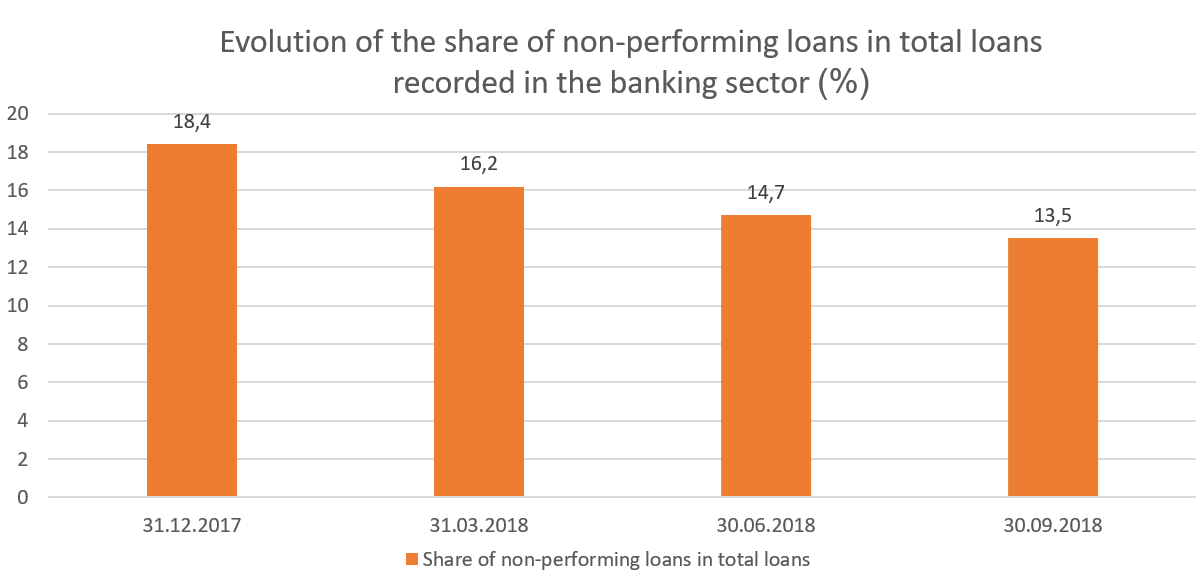

During the reference period, the share of non-performing loans (substandard, doubtful and compromised) in total loans decreased by 4.8 pp. compared to the end of 2017, recording 13.5% as of 30 September 2018. It should be noted that this indicator diminished across all banks, ranging from 5.1% to 33.2%. The decrease of the share of non-performing loans in total loans has been caused by the implementation of measures established by banking strategies on the reduction of the volume of non-performing loans, among which: to sell collaterals, to cooperate with specialized real estate agencies with a view to identifying potential buyers for pledged / mortgaged assets, etc.

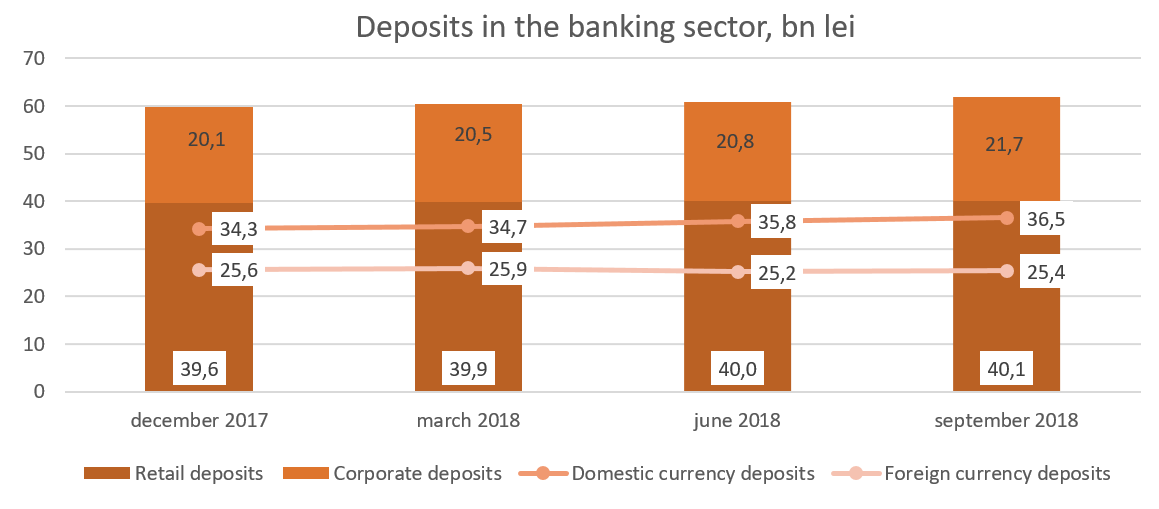

At the same time, the banking sector continued to record an upward trend in the balance of deposits. According to prudential reports, it increased by 3.4% in the reference period, amounting to MDL 61.9 billion (retail deposits accounting for 64.8% of total deposits, corporate deposits – 35.0% and deposits of banks – 0.2%). The increase in corporate deposits by MDL 1.6 billion (7.7%) had the biggest impact on the growth of the balance of deposits. The balance of retail deposits has increased by MDL 512.7 million (1.3%).

Domestic currency deposits accounted for 59.0% of total deposits, their balance increasing by MDL 2.3 billion (6.6%), thus amounting to MDL 36.5 billion as of 30.09.2018. Foreign currency deposits accounted for 41.0% of total deposits, their balance decreased during the last nine months of 2018 by MDL 219.3 million (0.9%) and totaling MDL 25.4 billion. The decrease of foreign currency deposits has been caused by the negative fluctuation of the exchange rate in amount of MDL (-669.9) million. At the same time, foreign currency deposits amounting to MDL 479.3 million have been attracted.

Compliance with prudential requirements

Banks continue to maintain high liquidity ratios. Thus, the value of the long-term liquidity indicator (1st liquidity principle) recorded 0.7 (with threshold of ≤1), a level equal to the one of the end of 2017. Current liquidity for the sector (2nd liquidity principle) recorded insignificant changes, recording 54.5% (with threshold of ≥20%), meaning that more than a half of the banking sector's assets are liquid. It should be mentioned that the largest shares in total liquid assets are held by deposits with the NBM – 41.6%, liquid securities – 30.6% and net interbank money – 17.1%. During the reference period, the share of deposits at NBM increased by 5.5%, as a necessity to preserve the required reserves, due to the increase of funds attracted by banks and limit of required reserves by 2.5 pp. Moreover, the share of liquid securities decreased by 3.7 pp. and the share of net interbank funds decreased by 3.2 pp.

All banks comply with the 3rd liquidity principle reflecting the ratio between the actual adjusted liquidity and the required liquidity for each maturity band, which should not be less than 1.

On 30 July 2018, the new regulations regarding the Basel III requirements entered into force (under the European CRD IV/CRR package) and the Guidelines on the submission by banks of COREP reports for supervisory purposes, which sets forth the requirements for the calculation of own funds by diminishing them not only with credit risk exposures, but also by considering the market risk, the operational risk and the settlement risk. In addition, the new regulations set the amount of capital buffers which shall attenuate the impact on own funds.

Therefore, according to the reports submitted by banks, on 30.09.2018, the share of total own funds of the banking sector amounted to 27.9%, which represents a decrease of 3.5 pp. compared to the data of 31.12.2017, while the transition to Basel III (July compared to June) had an impact of 5 pp., which falls in the limits of the calculation of impact of transition to Basel III, that has been previously performed by the NBM. The regulated limit is respected by every bank and may vary between 20.0 to 65.9%.

As of 30.09.2018, the total own funds amounted to MDL 11.0 billion and recorded a growth of 4.1% (MDL 436.4 million) during the reference period. The growth of own funds has been determined by including in the calculation of own funds the intermediary profits which have been obtained by banks before the entry into force of the Regulation on bank’s own funds and capital requirements. At the same time, due to prudential filters, the adjustments of basic 1st level own funds decreased by MDL 343.2 million. Moreover, the subsidiary of a foreign bank has distributed capital in amount of MDL 133.9 million. Also, the net intangible assets decreased by MDL 38.7 million.

Regarding the Regulation on large exposures, it should be noted that one bank still does not comply with the prudential limit of 15% of the total regulatory capital set by the NBM. However, the bank has developed the exposure reduction plan and meets the milestones set therein. In addition, there is one bank that did not respect the indicator set on 30 September 2018, because of a temporary situation that occurred regarding the transaction for the modification in the structure of ownership. Considering that the above-mentioned transaction was finished in October 2018, on the next management date, the bank shall comply with the limits set by the above-mentioned regulation.

In addition, one bank continues to breach the prudential limit of 30% set for the indicator “Report of ten largest net debts on credit and total credit portfolio and contingent liabilities included in the ten largest debts” because of a significant reduction of the loan portfolio of a bank.

Following the NBM’s presumption of banks’ related parties in accordance with relevant legislative changes, it was found that three banks have breached the prudential limit of 20% of the Tier 1 capital set for total exposure to related parties and groups of persons linked together with related parties, and the limit of 10% of the total regulatory capital set for the maximum exposure to a related party. Based on the NBM’s decision, the aforementioned banks submitted their remedial action plans containing measures to be applied that would ensure the banks’ compliance with applicable prudential limits as well as the improvement of their related party identification and monitoring processes. The plans were examined and approved by the NBM. The banks submit quarterly reports on the undertaken measures.

Income and profitability

As of 30.09.2018, the profits earned in the banking sector totaled MDL 1.3 billion, having decreased by 5.7% compared to the same period of the previous year.

Total income amounted to MDL 5.1 billion , out of which, interest income accounted for 63.0% (MDL 3.2 billion), and non-interest income - 37.0% (MDL 1.9 billion). At the same time, total expenditure amounted to MDL 3.8 billion, including interest expenses – 29.4% (MDL 1.1 billion) and non-interest expenses – 70.6% (MDL 2.7 billion).

The decrease in profits was caused by the decrease in the interest income by 10.1% or by MDL 362.7 million, as a result of the decrease of interest rate, as well as by the rise of non-interest expenses by 4.0% or MDL 103.9 million. Significant shares in non-interest income are held by income from fees and charges - 63.0%, income from foreign exchange differences – 32.4% (income from foreign currency trading and revaluation), other operating income - 4.5%.

Interest expense decreased by 22.7% or MDL 326.4 million, as a result of the decrease in the average deposit rate.

As of 30 September 2018, return on assets and return on capital recorded 2.1% and 12.7%, increasing by 0.2 pp. and 1.3 pp., respectively, compared to the end of the previous year.

Developments in the national legislative framework and its alignment with the EU legislation

During first 9 months of 2018, following the entry into force of the Law no. 202 of 06.10. 2017 on the Banking activity, the National Bank of Moldova:

-

has approved 8 regulations (regulatory acts), with regard to the requirements for the own funds and treatment of credit risks, market risks and operational risks, settlement/delivery risks in the context of own funds, as well as the requirements for capital buffers;

-

has approved the Guidelines on the submission by banks of COREP reports for supervisory purposes, which sets forth uniform requirements for reporting for supervisory purposes as well as specific requirements for reporting of data on own funds and risk exposures;

-

has approved the Regulation on external audit of banks, which sets the requirements for conducting an external auditing of the financial statements and for other purposes;

-

has modified the regulatory framework regarding the holding of participation share in the share capital of the bank, which refers to improving the access mechanisms on the banking financial market for persons, including from the countries which apply supervisory and prudential regulation requirements, at least similar with those applied in Moldova and which comply with the legal requirements on the quality of the banking shareholding structure;

-

has adjusted the examination process for receiving the prior approval of the National Bank of Moldova, regarding the acquisition or increase of shareholding in a bank.

Regarding the regulatory acts of own funds and treatment of above-mentioned risks, they have been elaborated under the Directive 2013/36/EU and Regulation 575/2013, which implement the Basel III international regulatory framework. Therefore, by implementing the respective regulatory acts, new approaches for the calculation of own funds and the rates of own funds (risk weighted capital adequacy) are promoted, which in addition to credit risk includes other risks, such as operational, market, settlement / delivery risks.

The National Bank of Moldova continues developing regulatory acts to ensure full application of the provisions of the Law no. 202 of 06.10. 2017 on the Banking activity.

The alignment of the banking legislation of the Republic of Moldova with international standards by means of improving the quantitative and qualitative mechanisms of banks’ management will contribute to the promotion of a secure and stable banking sector, to an increased transparency, trust and attractiveness of the domestic banking sector for banks’ potential investors and creditors, as well as for depositors, the development of new financial products and services.