Pursuant to its commitments to development partners, the National Bank of Moldova continues the process of promoting reforms in the banking sector, in particular setting a transparent shareholder structure to attract new strong investors, adequate assessment of bank's management and identification of transactions concluded with banks’ related parties. At the same time, the implementation of Basel III standards will allow the increase of safety and soundness of the banking sector, respectively strengthening its resistance to shocks and crises. Also, taking into account that the operational risk associated with information technologies (IT) is increasing and may lead to substantial losses, the National Bank of Moldova has requested from banks to carry out complex external audits in the IT domain.

On September 30, 2017, 11 banks licensed by the National Bank of Moldova (NBM) were operating in the Republic of Moldova, including 4 subsidiaries of foreign banks and financial groups.

During the first 9 months of 2017, the assets of the banking sector continued to register growth, the banks maintaining capital, liquidity and profitability at a high level. At the same time, the non-performing loans recorded a slight increase. Also, the declining trend of the lending activity is being kept..

National Bank of Moldova’s actions related to banks under intensive supervision and subject to early intervention

Pursuant to the finding of some indices related to shareholders’ non-transparent structure and engagement in high-risk lending operations, according to the Law on Financial Institutions, the National Bank of Moldova placed 3 banks under special supervision procedure (BC “MOLDOVA-AGROINDBANK” S.A., B.C. “VICTORIABANK” S.A. and BC “Moldindconbank” S.A.) on11.06.2015. Due to the amendment of the legislation, special supervision was replaced by intensive supervision and on 20.10.2016, intensive supervision placed on BC “Moldindconbank” S.A. was replaced by early intervention. It should be noted that these 3 banks hold 64.6 percent of total assets of the banking sector.

In June 2015, the National Bank of Moldova ordered to the banks concerned to employ an audit company to carry out a diagnostic study. Thus, in June 2016, following the diagnostic study’s results, the National Bank of Moldova adopted decisions on prescribing elaboration of Remedial Action Plans for the BC"MOLDOVA-AGROINDBANK" S.A. and for the B.C. "VICTORIABANK" S.A., obliging the banks, by the end of 2016, to remove all identified shortcomings. The banks took a range of measures to improve the core domains of activity, namely: monitoring of shareholders and bank’s related parties, corporate governance, lending activity, risk management, money laundering prevention domain, IT domain, and others.

At the same time, for the purpose of non-admitting excessive risks, the National Bank, on a daily basis, monitors the activity of banks under intensive supervision and under the early intervention regime. In such a way, is being examined the financial situation of the concerned banks, their transactions, the agenda of governing body’s’ meetings, etc.

The specified banks are well-capitalized and operate in normal regime (provide all services, including those concerned with deposits, loans and settlement operations).

In June 2017, the National Bank of Moldova initiated the identification by a foreign audit company of transactions concluded with related parties of the BC "MOLDOVA - AGROINDBANK" S.A., B.C. "VICTORIABANK" S.A. and BC ,,Moldindconbank" S.A. The reports on identification of transactions concluded with related parties by the specified banks have been received by the NBM and are going to be analyzed in order to take decisions..

BC „MOLDOVA – AGROINDBANK” S.A.

Concerning the finding of the National Bank of Moldova of two groups of shareholders of the BC “MOLDOVA-AGROINDBANK” S.A. who acted in concert and purchased a substantial quota in the share capital of the bank amounting to 43.1 percent, without prior written permission of the National Bank, they were about to alienate purchased shares within 3 months. Due to the fact that the aforementioned shares had not been alienated in the established deadline, they were cancelled and new ones were issued. In such a way, two new unique share packages were put for sale at the Moldova’s Stock Exchange till June 2017. On 20.06.2017, the National Commission for Financial Markets extended by 6 months the deadline for selling the bank’s newly issued shares. It should be noted, that several potential investors are interested in purchasing these share packages.

In the period of January – February, a full scope inspection on its activity was carried out at the bank. Following the approval of the Decision on the results of the full scope inspection by the Executive Board of the NBM on 29.06.2017, the bank is going to report quarterly to the National Bank on the implementation of measures to remove the drawbacks identified during the full scope inspection, including measures on consolidation of the internal control system related to lending activity, to transactions with related parties, and to corporate governance within the bank. The National Bank actively monitors the implementation by the bank of the prescribed measures.

B.C. „VICTORIABANK” S.A.

Within the intensive supervision of the B.C. "VICTORIABANK" S.A., the NBM pays increased attention to transparency of shareholders and right classification of assets according to the risk they bear. For this purpose, the NBM carries out the assessment procedure of the shareholders’ who hold substantial quotas in the capital of the B.C. "VICTORIABANK" S.A. and as a result, in March 2017, there were applied sanctions in the form of fine to certain holders of quotas in the share capital of the B.C. "VICTORIABANK" S.A. in amount of about MDL 1 million, which was paid to the state budget.

Following the results of a full scope inspection at the bank, on October 4, 2017, the Executive Board of the NBM approved the decision to apply the sanction in the form of fine to members of the Board of Directors of B.C. "VICTORIABANK" S.A., who were in the position during the period of inspection. The total amount of fines constitutes MDL 496.1 thousand. In particular, the bank did not comply with the prudential requirements related to lending activity, foreign currency regulations, risk concentration, assets classification, etc.

The bank was prescribed to develop a plan of remedial measures to liquidate the infringements and shortcomings found during the inspection by setting deadlines of fulfilment

BC „Moldindconbank” S.A.

Currently, the BC “Moldindconbank” S.A. is under early intervention regime which started on 20.10.2016, following the ascertaining of the concerted activity of a group of persons who purchased and holds a substantial share of the bank’s capital which amounts to 63.89 percent, without prior written permission of the NBM, infringing the provisions of the Law on Financial Institutions.

By the Decision from 20.10.2016, the NBM has nominated temporary administrators of the BC “Moldindconbank” S.A. To be noted, that by the NBM’s Executive Board Decision, as of 20.10.2017, the National Bank renewed by 3 months the designation period of temporary administrators of the BC “Moldindconbank” S.A.

Concerning the shares belonging to the group of persons, whose concerted activity was ascertained by the Decision of the Executive Board of the National Bank of Moldova no.278 of 20.10.2016 (63.89%), they were seized within a criminal case. Subsequently, during October 2017, the custodians and the registry company have informed the bank about lifting the seizure. Respectively, measures stipulated by legislation are to be taken.

At the same time, by the decision from October 20, 2016, the NBM has ordered the bank to conduct an assessment by an audit firm of its assets, liabilities and equity. Subsequently, by the Decision of the Executive Board of the NBM dating April 13, 2017, it was ordered to update the specified assessment and to present the final report to the NBM. The final assessment report was presented to the NBM in September. Currently, it is in the process of examination.

Also, as a result of on-site inspections carried out during the previous year at the BC "Moldindconbank" SA, the Executive Board of the National Bank, by the decision from April 13, 2017, requested the bank to prepare a plan of remedial measures to consolidate the management of credit and liquidity risk, to ensure that the risk-weighted capital adequacy ratio is maintained above 20 percent, to review the internal normative acts of the bank in order to improve them, etc.

In the second quarter of 2017, a full scope inspection on the bank’s activity was carried out. The report on the results of the inspection was sent to the bank in October, consequently in the following period the National Bank will issue a decision in this regard.

Also, in order to ensure rigorous monitoring of the bank which is under early intervention, the NBM requested from temporary administrators to periodically present the report on the financial situation of the bank and on the actions taken during the exercise of the mandates.

Financial situation of the banking sector and compliance with prudential regulations

As of 30.09.2017, the situation of the banking sector, based on the reports submitted by licensed banks, recorded the following trends:

Assets and liabilities

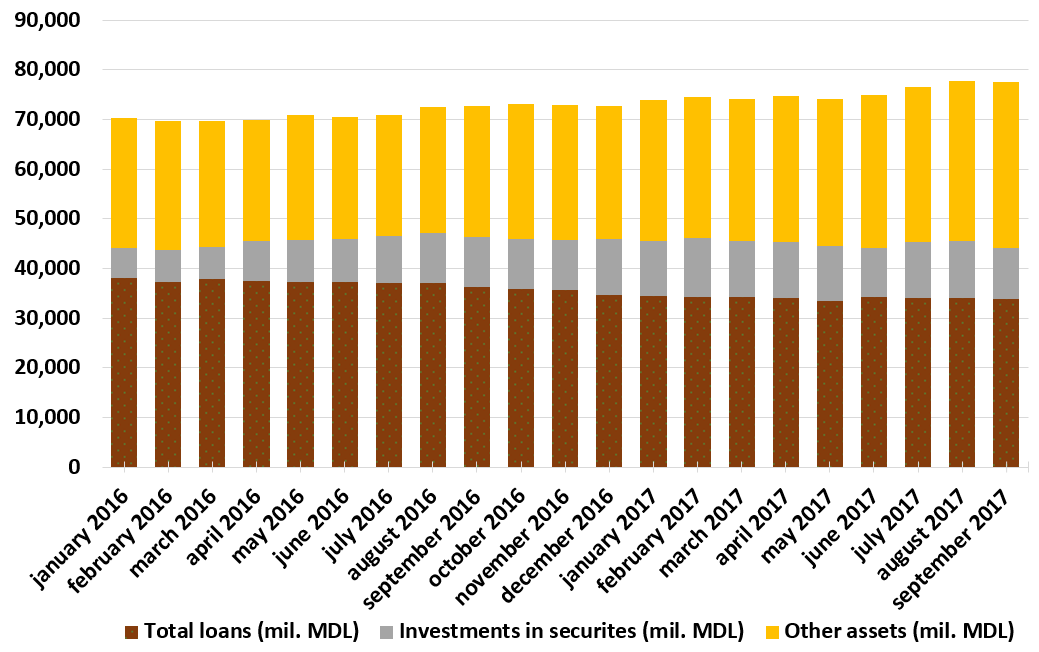

Total assets made up MDL 77.5 billion, increasing during 9 months of the year 2017 by 6.5 % (MDL 4.7 billion), mostly, due to the increase of liquid assets.

As at 30.09.2017, gross loan portfolio was 43.6 percent of total assets or MDL 33.8 billion, decreasing during 9 months of the year 2017 by 2.6 percent (MDL 919.4 million), including the III quarter – by MDL 374.7 million or 1.1 percent.

Investments in securities (certificates of the National Bank and government bonds) recorded a share of 13.2 percent of total assets, by 2.1. percentage points smaller than at the end of 2016, as a result of the decrease of base rate from 9 percent to 7.5 percent.

The rest of assets, which makes up 43.1 percent, are maintained by banks in the accounts opened at the National Bank, other banks, in cash, etc.

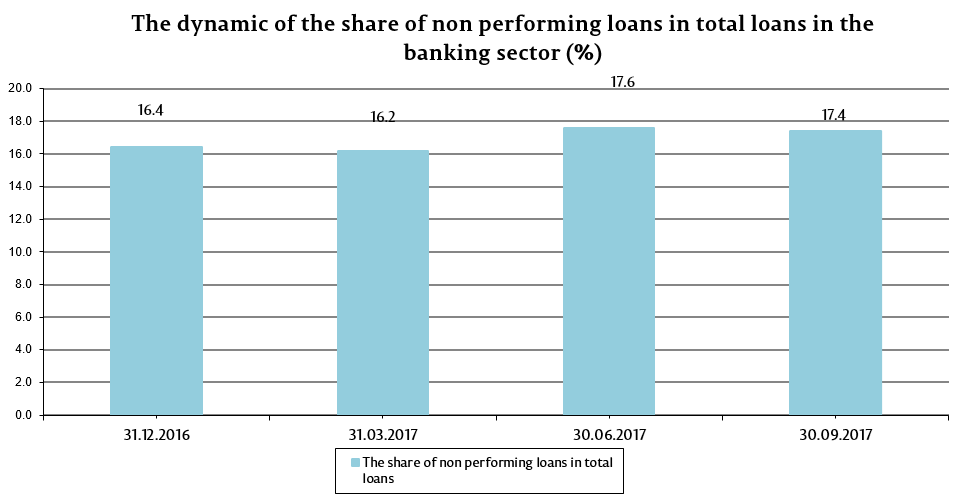

During the 9 months of the year 2017, the share of non-performing loans (substandard, doubtful and compromised) in total loans increased by 1.0 percentage points compared with the end of the year 2016, making up 17.4 percent on 30.09.2017, following reclassification of loans to non-performing risk categories as a result of the NBM inspections. The specified indicator varies from one bank to another, the highest value constituting 33.7 percent. Compared to June 30, 2017, the share of non-performing loans in total loans declined slightly. The positive dynamics in the third quarter of 2017 is due to the actions taken by banks to reduce bad loans, in accordance with recommendations of the National Bank of Moldova on continuous monitoring of loans’ quality, promotion of good governance and strengthening internal credit risk policies and strategies.

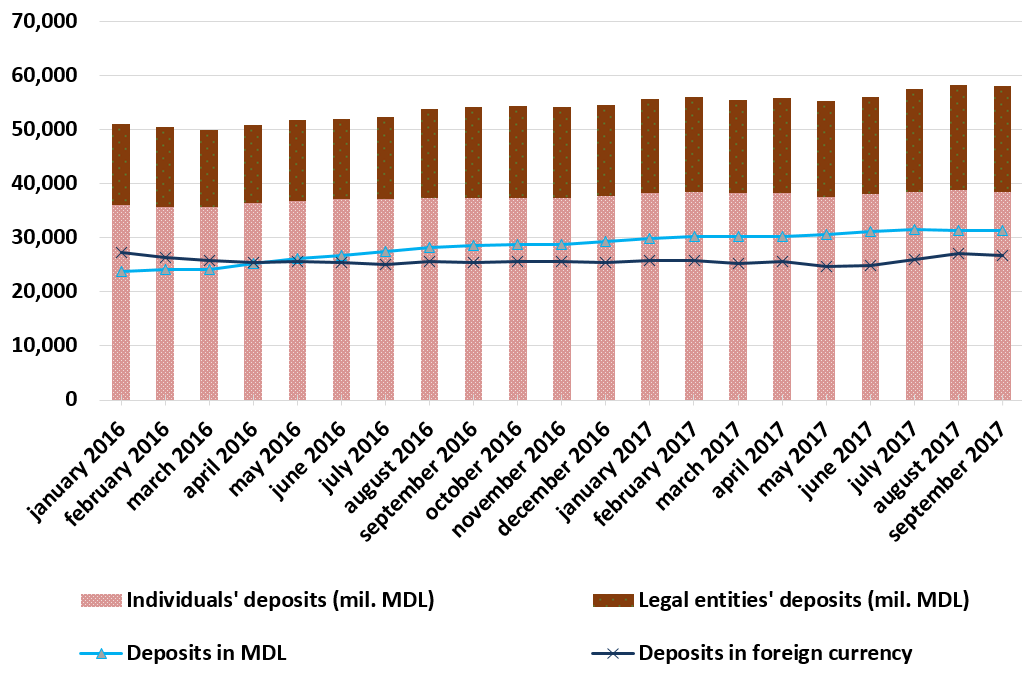

During the first 9 months of 2017, in the banking sector continued the trend of deposits increase. According to prudential reports, they increased by 6.1% in the reference period, amounting MDL 58.2 billion (individuals’ deposits represented 66.2% of total deposits, legal entities’ deposits - 33.6% and banks’ deposits - 0.2%). The biggest impact on the increase of deposits was the increase of legal entities’ deposits by MDL 2.6 billion (15.0%). Also, the individuals’ deposits increased by MDL 839.9 million (2.2%). At the same time, the banks’ deposits decreased by MDL 51.7 million (30.1%).

Also, the deposits in MDL continued to increase and during the first 9 months of 2017 went up by MDL 2.1 billion (7.0 percent) up to MDL 31.4 billion, the increase being also recorded for the foreign currency deposits - by MDL 1.3 billion (5.0 percent) up to MDL 26.8 billion.

Compliance with prudential requirements

The banks maintained the liquidity indicators at a high level. Thus, the long-term liquidity indicator value (principle I of liquidity) accounted for 0.6, being at the same level recorded at the end of 2016. Current liquidity (principle II of liquidity) increased by 3.9 p.p., representing 53.2%, so more than half of the banking sector assets are concentrated in liquid assets. It is worth mentioning that the largest increase in the structure of liquid assets during the first 9 months of 2017 was registered at interbank resources - by 29.0%, cash - by 28.4%, as well as at the accounts opened at the NBM - by 23.1% (including as a result of increase of the required reserve norm).

High level of risk-weighted capital adequacy ratio (average per sector - 30.7 percent, regulated limit for each bank ≥16 percent) allowed banks to absorb losses related to worsening of loan quality. At the same time, all banks comply with the regulated limit, which varies from 23.8 percent to 100.0 percent.

As of 30.09.2017, the Tier one capital amounted to MDL 10.2 billion and during the mentioned period it recorded an increase of 9.8% (MDL 911.4 million). The increase of the Tier I capital was mainly determined by obtaining the profit of MDL 1.4 billion. At the same time, the following factors influenced negatively the increase of the capital: increase by MDL 158.4 million of the calculated amount but unreserved of allowances for impairment losses on assets and contingent liabilities; formation by a bank of additional depreciation on assets in the amount of MDL 191.9 million, following the external audit and he NBM inspections; distribution by a bank (subsidiary of the foreign bank) of dividends in amount of MDL 163.2 million.

It should be noted that, previously, the NBM requested banks to adopt a more prudent and conservative policy concerning distribution of dividends.

According to the reports submitted on 30.09.2017, the banks comply with the Regulation on bank’s related parties. However, indicators reported by banks may change as a result of the examination of the audit firm's report on transactions with related parties of banks under intensive supervision and in early intervention regime.

Regarding the Regulation on “large” exposures it should be mentioned that two banks exceed the limits set by the NBM. One bank is still violating the 15 percent limit of total regulatory capital related to maximum exposure, however, this bank has a plan of reduction of exposure, in compliance with the deadlines set out in the plan. Another bank violates the exposure ratio to shareholders who manage, directly or indirectly, or control less than 1% of the share capital of the bank, including their related parties, in the total regulatory capital of the bank (regulated limit ≤20%, reported beginning with 30.06.2017), it represented 25 percent on 30.09.2017, being in decrease compared to the previous quarter.

Income and profitability

On 30.09.2017, the profit amounted MDL 1.4 billion and in comparison with the similar period of the previous year it increased by 3.8 percent.

Profit increase is determined by the decrease by 39.1 percent of interest expenses (from deposits) and by increase of non-interest income by 4.6 percent (mostly from fees and taxes – increase by 11.0 percent). A significant share in non-interest income represent income from taxes and fees - 61.1 percent.

Net income from taxes and fees amounted MDL 777.2 million and registered an increase of 7.9 percent during the period of 30.09.2016 – 30.09.2017.

Interest income amounted MDL 3.6 billion, decreasing by MDL 1.24 billion compared to the similar period of the precedent year. It was generated, in particular, by loans and debts (MDL 2.9 billion).

On 30.06.2017, return on assets and return on equity recorded 2.4 percent and 14.3 percent respectively (increasing by 0.6 and 3.2 percentage points respectively).

Development of the national legislative framework and its alignment to the EU framework

On October 6, 2017, the Parliament approved in final reading the draft Law on banks’ activity, which will enter into force on January 1, 2018 (implementation will be performed in stages till 2020). The Law on banks’ activity will strengthen the banking regulatory and supervision framework by aligning to European standards (including the transition from Basel I to Basel III).

For the purpose of final analysis of the level of preparedness of the banking sector in the context of transition to Basel III capital requirements, the National Bank initiated an impact survey, the first pillar, which aims to determine the quantitative and qualitative impact of regulations on the regulated level of banks’ capital.

After the publication of the new banking law in the Official Monitor of the Republic of Moldova, the draft secondary regulatory framework under the Law on banks’ activity (more than 20 regulations) and the COREP reporting framework, which will come into effect in stages, will be subject to public consultation. The specified regulations were developed within the EU Twinning Project related to strengthening the capacity of the NBM in the domain of banks regulation and supervision in collaboration with the Central Bank of Netherlands and the National Bank of Romania.

It should be noted that the new regulatory framework will keep some current prudential provisions and will focus, predominantly, on strengthening of the internal corporate governance and risk management practices in banks. New approaches will also be introduced for the calculation of regulatory capital, risk-weighted capital adequacy (which will include, besides the credit risk other risks - operational, market and other risks related to banking activity) and liquidity ratios. In addition, new concepts will be introduced such as leverage ratio, capital buffers, the internal capital adequacy assessment process (ICAAP) and the internal liquidity adequacy assessment process (ILAAP), disclosure requirements.

By the implementation of the law, the National Bank of Moldova, will carry out a fundamental review of the banking supervision system, using the supervisor’s arguments based on risk, provisioning and approach of the supervision review and assessment process (SREP). The NBM will possess a range of tools in order to apply the supervisory and remedial measures. Prudential supervision will be carried out including a consolidated basis, on a tight cooperation with foreign supervisors (including participation in supervision panels) and other competent authorities.

In order to improve the corporate governance in banks, on July 1, 2017, the Regulation on Internal Governance and Risk Management in Banks entered into force, with provisions concerning the risk management, requirements on policies for risk management and limits on risk appetite and risk profile, which ensure a gradual transition to the transposition package of the Basel III framework.

At the same time, in order to improve the system of continuous promotion for the position of administrator within banks of persons who correspond to the fit and proper principle and, respectively, to ensuring efficient management of the bank, on 27 July 2017 the new version of the Regulation on requirements to bank administrators was approved. The amendments provide for improvement of the qualification and experience criteria of the proposed person for the position of administrator, the assessment being carried out by the bank and the supervisor for each person, by applying the judgments on the basis of significant information related to all the evaluation criteria and taking into account any other relevant circumstances, including the size of the bank, the nature and complexity of its activity.

At the same time, the alignment of the Republic of Moldova’s legislation in this field to the applicable international standards will contribute to the attractiveness of the domestic banking sector to foreign investors, to the development of new financial products and services, having more safe and strong banks, that play an important role in financial intermediation.

In conclusion, the new legislation will lead to the improvement of the quantitative and qualitative mechanisms of banks’ management, consolidation of the domestic banking system, increase in the public’s confidence, ensuring financial stability of the Republic of Moldova.