Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

During the first quarter of 2023, the banking sector successfully faced external challenges. The National Bank of Moldova (NBM) continued the process of prudential supervision of banks, following the legal requirements, in order to ensure the stability and viability of the banking system.

The financial situation of the banking sector, according to data submitted by banks, is characterised by growth in assets and deposits of natural and legal persons. The profit for the year compared to the same period of the previous year increased mainly as a result of higher interest and non-interest income. Interest income increased, mainly due to income from investments in debt securities (G-Sec, NBC). Income from lending and income from funds placed with the NBM (required reserves) also showed growth.

At the same time, there was a decrease in the absolute value of outstanding loans and non-performing loans, and the loan portfolio quality indicators remained almost at the same level as at the end of the previous year.

Simultaneously, loans, own funds, the own funds ratio, and deposits of banks decreased insignificantly.

As of March 31, 2023, 11 banks licensed by the National Bank of Moldova were active in the Republic of Moldova.

As of March 31, 2023, the situation in the banking sector, reflected by the reports submitted by banks, registered the following trends:

Assets and liabilities

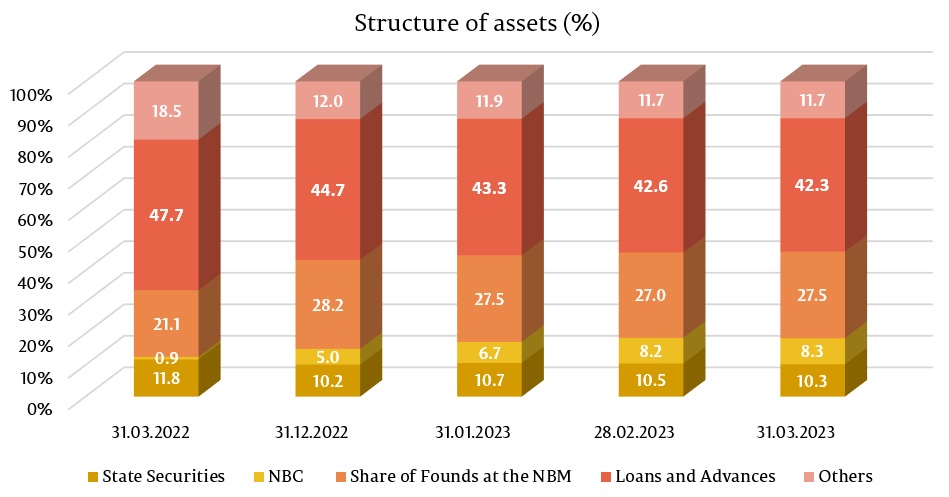

Total assets amounted to MDL 138.3 billion, increasing by 5.2% (MDL 6.8 billion) during the first quarter of 2023.

The largest share in total assets went to "Loans and advances at amortized cost" which amounted to 42.3% (MDL 58.5 billion), decreasing by 2.4 percentage points (pp) compared to the end of the previous year.

The share of funds at the NBM was 27.5% (MDL 38.0 billion), decreasing by 0.7 pp, and the share of banks' investments in state securities and National Bank certificates accounted for 18.6% (MDL 25.6 billion), increasing by 3.4 pp. The rest of the assets, which account for 11.7% (16.2 billion), are kept by banks in other banks, in cash, tangible fixed assets, intangible fixed assets, etc. Their share decreased by 0.3 p.p. compared to the end of the year 2022.

The gross (prudential) balance of loans accounted for 44.2% of total assets, or MDL 61.6 billion, decreasing during the period under review by 0.8% (MDL 505.6 million).

The largest decrease during the first quarter of 2023 was recorded in loans granted to trade - by MDL 284.8 million (2.1%) to MDL 13.6 billion; loans granted to consumers - by MDL 257.6 million (2.6%) to MDL 9.8 billion; loans granted to the energy industry - by MDL 194.2 million (20.9%) to MDL 733.1 million; loans granted for the purchase / construction of real estate – by MDL 155.1 million (1.3%) up to MDL 12.1 billion; loans granted to the food industry - by MDL 96.0 million (2.2%) up to MDL 4.3 billion; and loans granted to the productive industry by MDL 68.5 million (2.6%) to MDL 2.6 billion.

At the same time, the largest increase was recorded in loans granted in the field of service provision, which amounted to MDL 147.1 million (6.4%) to MDL 2.4 billion; in loans granted to agriculture - by MDL 134.7 million (3.0%) to MDL 4.6 billion and in loans granted to individuals engaged in business - by MDL 131.9 million (8.1%) to MDL 1.8 billion.

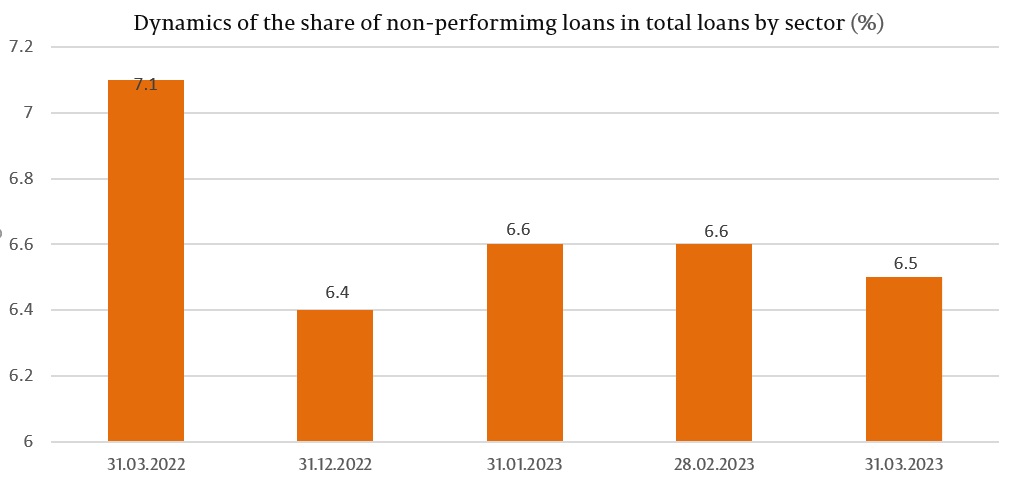

During the reference period, the share of non-performing loans (substandard, doubtful, and compromised) in total loans increased insignificantly by 0.1 pp, accounting for 6.5% on March 31, 2023, with the indicator ranging from 1.8% to 9.2%, depending on the bank.

At the same time, non-performing loans in absolute value decreased by 0.2% (from MDL 9.1 million) to MDL 4.0 billion.

During the period under review, the share of expired loans decreased by 0.5% (from MDL 9.8 million) up to MDL 2.0 billion. The share of expired loans in total loans was 3.3%, being at the same level as on March 31, 2023, ranging from 0.1% to 8.7%, depending on the bank.

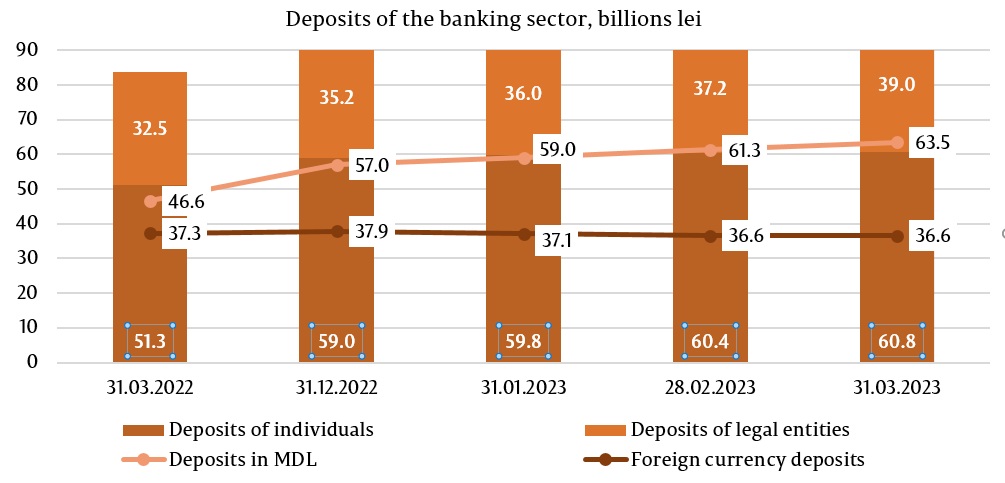

At the same time, during the reference period, the total balance of deposits increased by MDL 5.2 billion, or by 5.5%, amounting up to MDL 100.2 billion (deposits of individuals accounted for 60.7% of total deposits, deposits of legal entities – 38.9% deposits of banks – 0.4%), as a result of the increase in the balance of deposits of legal entities by MDL 3.8 billion (10.7%) up to MDL 39.0 billion and deposits of individuals by MDL 1.7 billion (2.9%) up to MDL 60.8 billion. At the same time, the balance of bank deposits decreased by MDL 319.3 million (41.6%) up to MDL 447.6 million.

In total deposits, 63.4% went to deposits in MDL, their balance increasing by MDL 6.5 billion (11.4%) compared to the end of the previous year and amounted to MDL 63.5 billion on March 31, 2023. Foreign currency deposits accounted for 36.6% of total deposits, their balance decreased during the reference period by MDL 1.3 billion (3.4%), making up MDL 36.6 billion (withdrawal of foreign currency deposits - equivalent to MDL 382.9 billion, negative revaluation of foreign currency deposits – MDL 901.2 billion).

Revenues and profitability

As of March 31, 2023, the profit in the banking system amounted to 1.3 billion lei, increasing by 67.3% (MDL 538.5 billion) compared to the end of the previous year.

The increase in profit was due to the increase in interest income by MDL 1.8 billion (104.4%) and non-interest income by MDL 94.8 million (8.8%) At the same time, interest expenditure increased by MDL 862.6 million (234.4%) and non-interest expenses (expenses related to fees and commissions, administrative expenses, provisions, impairment of financial and non-financial assets, etc.) by MDL 455.3 million (28.6%).

Total revenues amounted to MDL 4.6 billion, increasing compared to the end of the previous year by MDL 1.9 billion (67.3%), of which interest income amounted to MDL 3.4 billion (74.7% of total revenues), and non-interest income – MDL 1.2 billion (25.3% of total revenues).

At the same time, total expenditure amounted to MDL 3.3 billion, increasing compared to the similar period of the previous year by MDL 1.3 billion (67.3%), of which interest expenditure was MDL 1.2 billion (37.6% of total expenditure), and non-interest expenditure – MDL 2.0 billion (62.4% of total expenditure).

As of March 31, 2023, return on assets accounted for 3.8%, increasing by 0.9 p.p. and return on capital accounted for 22.1%, increasing by 5.1 pp compared to the end of the previous year.

Compliance with prudential requirements

During the first quarter of 2023, banks continued to maintain liquidity indicators at a high level, above regulated limits.

Thus, the value of the long-term liquidity indicator (liquidity principle I) was 0.66 (limit ≤1), ranging from 0.32 to 0.75, depending on the bank, being almost at the same level as at the end of 2022.

Liquidity Principle III, which is the ratio of adjusted effective liquidity to required liquidity on each maturity band and which should not be less than 1 on each maturity band, has also been complied with by all banks, ranging from 1.34 on the maturity band up to one month inclusive up to 160.12 on the maturity band between one month and three months inclusive.

The liquidity coverage ratio by sector amounted to 287.0% (limit ≥ 100% - from January 1, 2023), ranging from 210.9% to 572.5%, increasing by 77.3 pp compared to the end of the year 2022.

According to the reports presented by the banks as of March 31, 2023, the total own funds ratio in the banking sector registered a value of 29.0%, decreasing insignificantly by 0.1 pp compared to the end of the previous year, ranging from 21.8% to 59.1%. All banks met the indicator "Total own funds ratio" (≥10%).

All banks also complied with the "Total Own Funds Ratio" indicator requirement, considering capital buffers.

As of March 31, 2023, total own funds amounted to MDL 18.3 billion and registered a decrease of 0.5% (MDL 86.5 billion). The decrease in own funds was mainly determined by the increase in the positive difference between allowances for losses on assets and contingent liabilities and the size of allowances for impairment losses on assets and provisions for losses.

As of March 31, 2023, the banks complied with the prudential indicators regarding large exposures and exposures to their affiliates, with the exception of one bank, where the limit of 15% of the maximum exposure amount to a client or to a group of connected clients/ Eligible Capital (≤15%) was exceeded, which amounted to 16.37%. The indicator returned to the prudential limit at the next monthly report.

During the first quarter of 2023, there were no normative acts approved to implement the provisions of Law No. 202/2017 on the activity of banks. At the same time, the NBM continues the activities related to the elaboration and submission of draft updates of secondary normative acts for the enforcement of Law 202/2017 and the promotion of Basel III requirements.