Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

The National Bank of Moldova continuously promotes reforms in the banking sector, focusing in particular on establishing a transparent shareholders structure in order to attract new and adequate investors, proper assessment of banks’ management, identification of transactions concluded with banks’ related parties and timely identification of non-performing loans.

The new Law on banks activity (based on Basel III principles) entered into effect on January 1, 2018. At the same time, the implementation of the new regulatory and supervisory framework will allow to increase the safety and soundness of the banking sector and respectively strengthen its resilience to shocks and crises, to strengthen internal governance, will ensure that all risks are registered in banks' reports while maintaining adequate capital both qualitatively and quantitatively, as well as will allow to provide more secure and qualitative financial services.

On December 31, 2017, 11 banks licensed by the National Bank of Moldova (NBM) were operating in the Republic of Moldova, including 4 subsidiaries of foreign banks and of financial groups.

During the year 2017, the assets of the banking sector continued to register growth, capital adequacy strengthened, the banks have excessive liquidity, and profitability of banks is at a high level. The banking sector faces problems related to the high level of non-performing loans in the loan portfolio and follow to make greater efforts to eliminate non-performing loans in their balance sheets. Also, the declining trend of the lending activity is being kept. At the same time, the banks are going to play a more active role in financing the country's economy.

Also, in order to prevent the risk associated with information technology (IT), which constitutes a major task, in 2017, the National Bank of Moldova required banks to perform a complex external audit in the IT field. The banks are expected to increase their investments in IT to prevent and mitigate this risk.

Pursuant to the finding of some indices related to shareholders’ non-transparent structure and engagement in high-risk lending operations, according to the Law on Financial Institutions, the National Bank of Moldova, on 11.06.2015, placed 3 banks under special supervision procedure (BC “MOLDOVA-AGROINDBANK” S.A., B.C. “VICTORIABANK” S.A. and BC “Moldindconbank” S.A.). Due to the amendments of the legislation, special supervision was replaced by intensive supervision, and on 20.10.2016, the intensive supervision regime on BC “Moldindconbank” S.A. was replaced by early intervention. It should be noted that these 3 banks hold 65.2 percent of total assets of the banking sector.

At the same time, for the purpose of non-admitting excessive risks, the National Bank, on a daily basis, monitors the activity of banks under intensive supervision and under the early intervention regime. In such a way, is being examined the financial situation of the concerned banks, their transactions, the agenda of governing organs’ meetings, etc.

The specified banks are well-capitalized and operate in normal regime (provide all services, including those concerned with deposits, loans and settlement operations).

In June 2017, the National Bank of Moldova initiated the identification by a foreign audit company of transactions concluded with related parties of the BC "MOLDOVA - AGROINDBANK" S.A., B.C. "VICTORIABANK" S.A. and BC “Moldindconbank” S.A. Soon, the National Bank will take a decision regarding the presumption of related parties to the three banks. Respectively, the banks are going to develop plans to comply with the decision of the NBM on related parties’ identification..

B.C. „VICTORIABANK” S.A.

Within the intensive supervision of the B.C. "VICTORIABANK" S.A., the NBM pays increased attention to transparency of shareholders and right classification of assets according to the risk they bear. For this purpose, the NBM carries out the assessment procedure of the shareholders who hold substantial quotas in the capital of the B.C. "VICTORIABANK" S.A. and as a result, in March 2017, there were applied sanctions in the form of fine to certain holders of quotas in the share capital of the B.C. "VICTORIABANK" S.A. in amount of about MDL 1 million, which was paid to the state budget. The mentioned shareholder with a 39.2 percent quota in the share capital of BC "VICTORIABANK" S.A. has decided to sell its share package.

On 16 January 2018, the auction on the regulated market of the Moldovan Stock Exchange took place, where the mentioned package of shares was sold. So, the investor became Banca Transilvania, the second largest bank in Romania, through the Dutch company VB Investment Holding B.V. As a result of the transaction, VB Investment Holding BV, which as of May 24, 2016 is a shareholder with 27.56 percent of the share capital of the bank in partnership with Banca Transilvania in Romania and the European Bank for Reconstruction and Development, will hold 66.77 percent of the bank's share capital. The new shareholder will contribute to improving corporate governance in the bank and of the internal control and respectively to improving the bank's business.

Following the results of a full scope inspection at the bank, on October 4, 2017, the Executive Board of the NBM approved the decision to apply the sanction in the form of fine to members of the Board of Directors of B.C. "VICTORIABANK" S.A., who were in the position during the period of inspection. The total amount of fines constitutes MDL 496.1 thousand. In particular, the bank did not comply with the prudential requirements related to lending activity, foreign currency regulations, risk concentration, assets classification, etc.

The Bank has developed a plan of remedial measures for liquidation of infringements and shortcomings found during the inspection by setting of concrete deadlines, which was examined by the NBM and the bank was required to supplement the plan with additional measures pertaining to: internal governance, transparency of shareholders, currency regulation, prevention and fighting money laundering, payment systems. The bank has to present the amended plan of actions and to report to the National Bank on its fulfilment on monthly basis..

BC „MOLDOVA – AGROINDBANK” S.A.

Concerning the finding of the National Bank of Moldova of two groups of shareholders of the BC “MOLDOVA-AGROINDBANK” S.A. who acted in concert and purchased a substantial quota in the share capital of the bank amounting to 43.1 percent, without prior written permission of the National Bank, they were about to alienate purchased shares within 3 months. Due to the fact that the aforementioned shares had not been alienated in the established deadline, they were cancelled and new ones were issued. In such a way, two new unique share packages were put for sale at the Moldova’s Stock Exchange till June 2017. The National Commission for Financial Markets extended for several times the deadline for selling the bank’s newly issued shares, the last deadline being till September 2018.

Following the full scope inspection carried out in the period January - February 2017 at the bank, the Decision of the Executive Board of the NBM was adopted, the members of the Supervisory Board of BC "MOLDOVA-AGROINDBANK" S.A. were sanctioned with warning, and the members of the Bank's Board of Directors with warning and fine in total amount of MDL 760.7 thousand. Similarly, according to the above decision, the bank has been prescribed a series of measures in order to improve lending and customer awareness, to improve regulatory standards in the field of crediting and internal control, the security management system, the internal control and payment system.

The bank is reporting quarterly to the National Bank on the implementation of measures to remove the drawbacks identified during the full scope inspection, including measures on consolidation of the internal control system related to lending activity, to transactions with related parties, and to corporate governance within the bank. The National Bank actively monitors the implementation by the bank of the prescribed measures.

BC „Moldindconbank” S.A.

Currently, the BC “Moldindconbank” S.A. is under early intervention regime which started on 20.10.2016, following the ascertaining of the concerted activity of a group of persons who purchased and hold a substantial share of the bank’s capital which amounts to 63.89 percent, without prior written permission of the NBM, in such a way infringing the provisions of the Law on Financial Institutions.

By the Decision from 20.10.2016, the NBM has nominated temporary administrators of the BC “Moldindconbank” S.A. As of January 20, 2018, the Executive Board of the National Bank of Moldova decided to renew for a 6 months’ period the mandates of temporary administrators of the bank.

Concerning the shares belonging to the group of persons, whose concerted activity was ascertained by the Decision of the Executive Board of the National Bank of Moldova from 20.10.2016 (63.89 percent), they were seized within a criminal case. Subsequently, during October 2017, the custodians and the registry company have informed the bank about lifting the seizure. In January 2018, in accordance with the legal provisions, the Board of Directors of the BC "Moldindconbank" S.A. approved the decision on the cancellation of a few of the shares issued by the bank and the issuance of certain new shares, amounting to 63.89 percent of the bank's share capital, which follow to be put on sale. Within a 3 months’ period, a recognized independent international company will determine the initial exposure price for newly issued shares and after that the shares will be put on sale at the Stock Exchange.

During the period of the early intervention regime, a range of on-site inspections were carried out by the NBM and external audit firms to assess the bank's financial situation. As a result, the bank prepared a plan of remedial measures to consolidate the management of loans and liquidity risk, to ensure that the risk-weighted capital adequacy ratio is maintained above 20 percent, to review the internal normative acts of the bank in order to improve them, etc.

Following the full scope on-site inspection performed at the bank, the Executive Committee of the NBM approved the decision by which it decided to sanction with warning BC "Moldindconbank" S.A. for violations admitted as a result of decisions taken and practices admitted until the appointment of temporary administrators, the most part of violations being remedied by 30.11.2017. Thus, the bank did not comply with prudential regulations regarding lending, risk concentration, asset classification, customer knowledge, payment services and payment and settlement systems. The bank is going to prepare a plan of remedial measures regarding the liquidation of the violations and shortcomings found as a result of the full scope on-site inspection, with setting concrete deadlines. The bank will present the plan to the National Bank.

Also, the NBM requested from temporary administrators to periodically present the report on the financial situation of the bank and on the actions taken during the exercise of the mandates.

As of 31.12.2017, the situation of the banking sector, based on the reports submitted by licensed banks, recorded the following trends:

Assets and liabilities

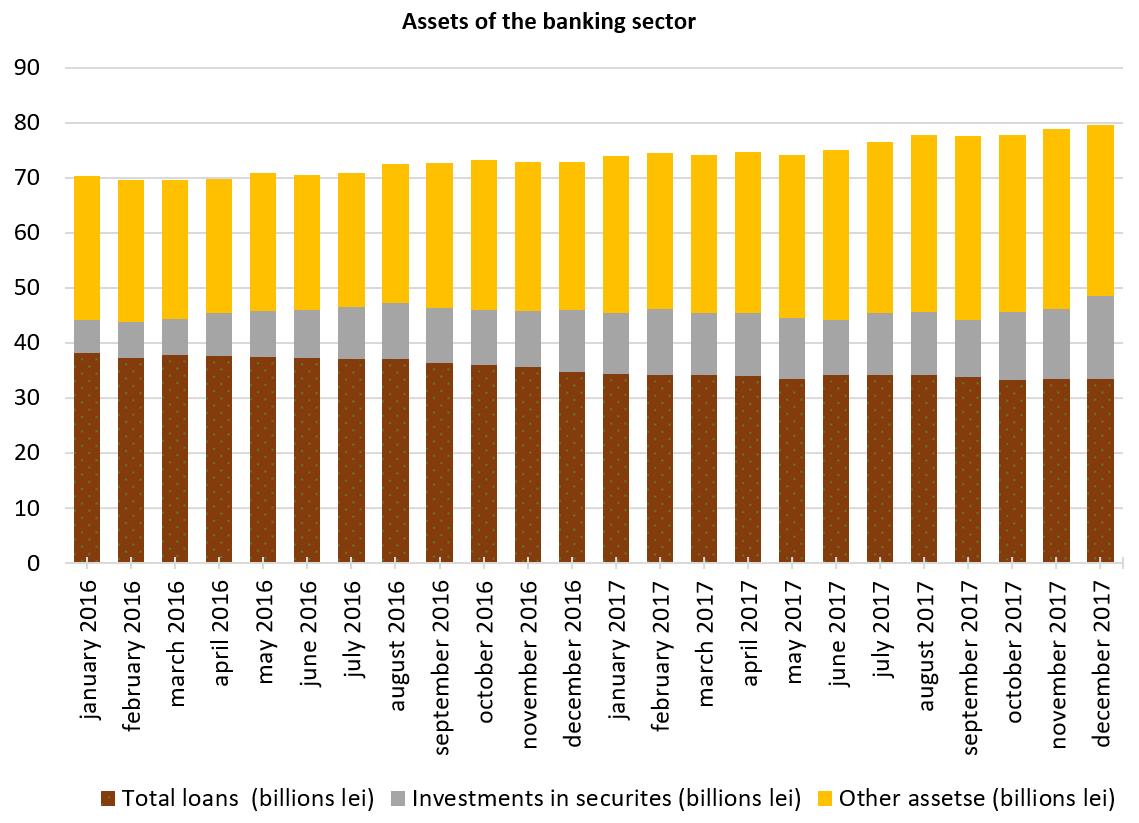

Total assets made up MDL 79.5 billion, increasing during the year 2017 by 9.2 percent (MDL 6.7 billion).

As at 31.12.2017, gross loan portfolio was 42.1 percent of total assets or MDL 33.5 billion, decreasing during the year 2017 by 3.7 percent (MDL 1.2 billion). The National Bank encourages banks to be more active in recovering deposits attracted at granting qualitative loans for the economy of the country. The volume of new credits granted in 2017 increased by 9.0 p.p. compared to 2016. The decrease of the interest rate for loans also had a positive influence on the increase in the volume of new loans.

Investments in securities (certificates of the National Bank and government bonds) recorded a share of 19.0 percent of total assets, being by 3.7. percentage points bigger than at the end of 2016.

The rest of assets, which make up 38.9 percent, are maintained by banks in the accounts opened at the National Bank, other banks, in cash, etc.

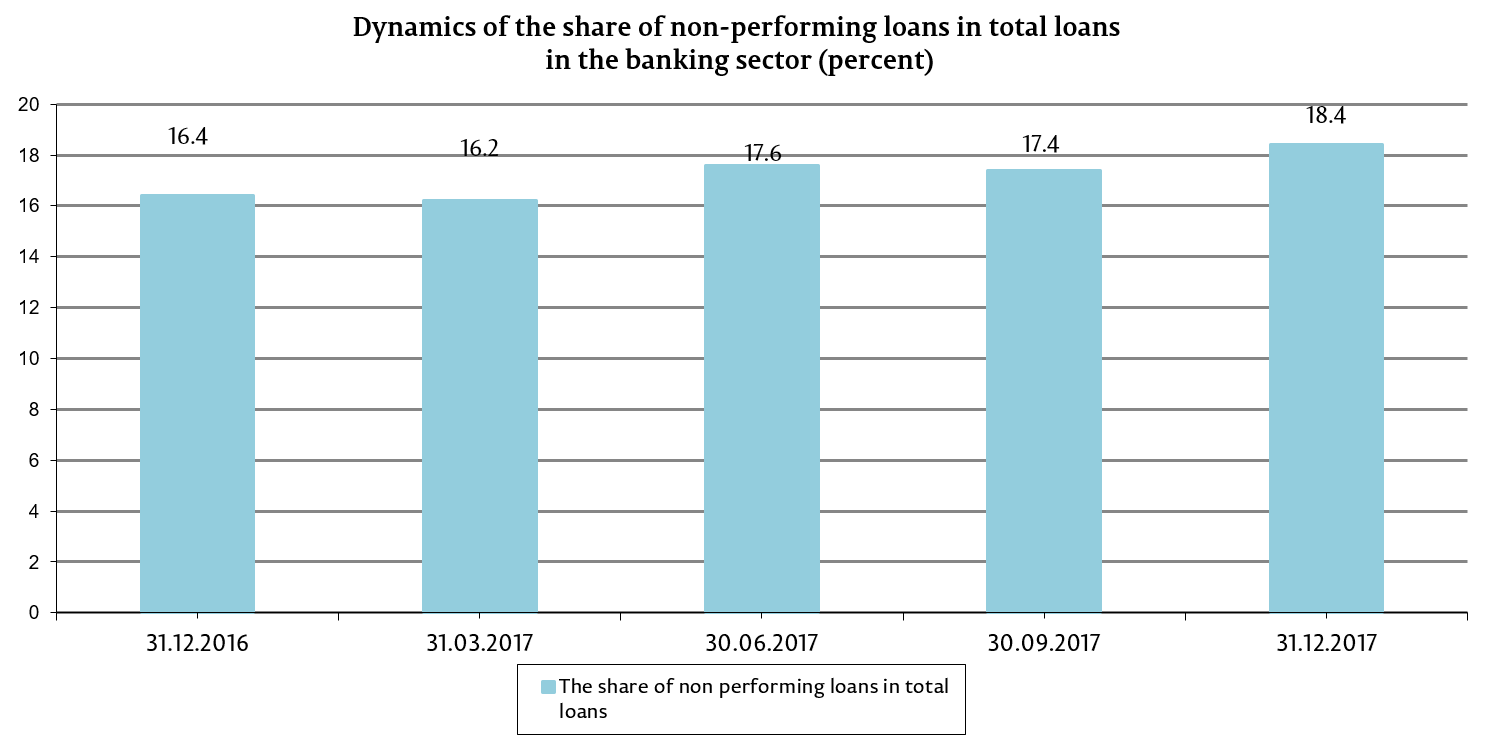

During the year 2017, the share of non-performing loans (substandard, doubtful and compromised) in total loans increased by 2.0 percentage points compared with the end of the year 2016, making up 18.4 percent on 31.12.2017. Reclassification of loans to non-performing risk categories took place as a result of a more prudent approach in classification of loans portfolio. The specified indicator varies from one bank to another, the highest value constituting 34.1 percent.

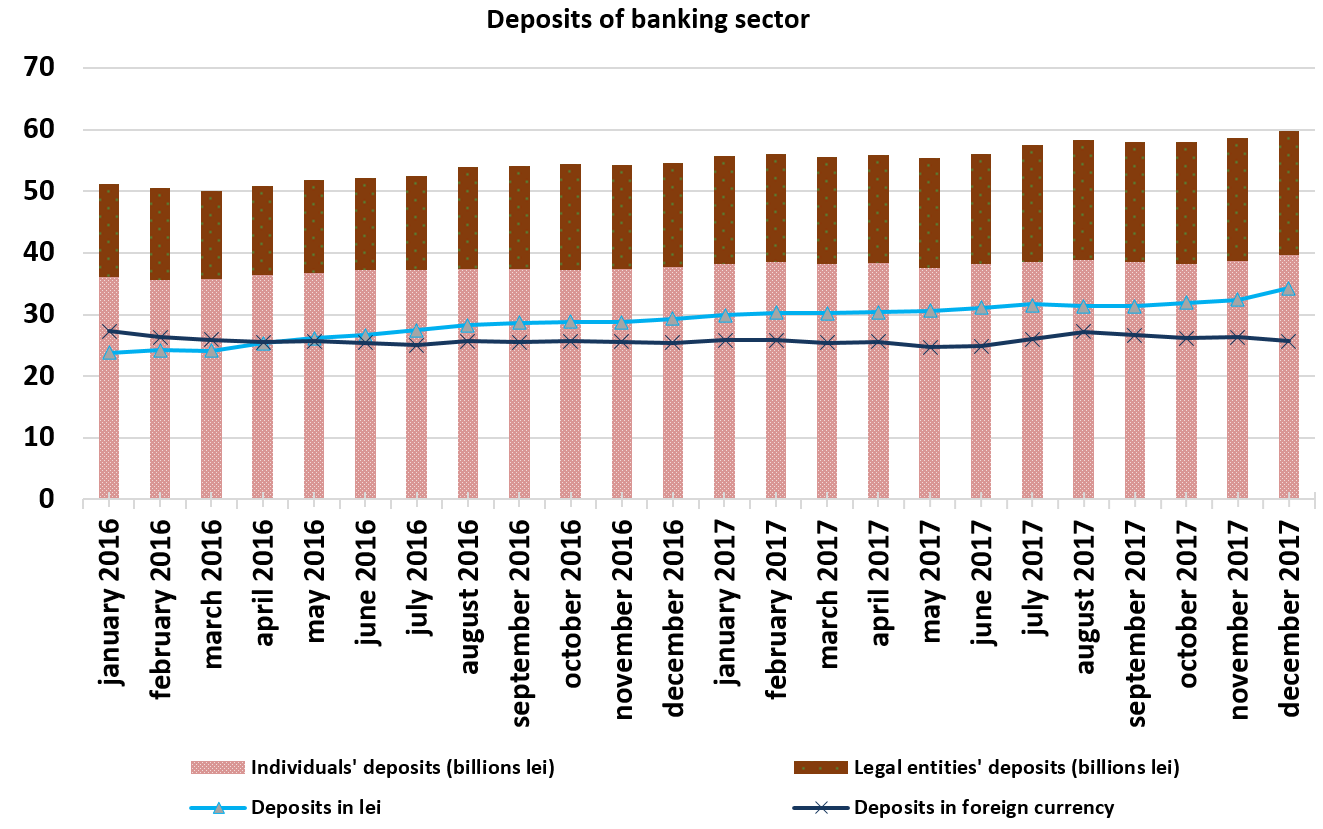

During the year 2017, in the banking sector continued the trend of deposits balance increase. According to prudential reports, they increased by 9.2 percent in the reference period, amounting to MDL 59.9 billion (individuals’ deposits represented 66.2 percent of total deposits, legal entities’ deposits - 33.6 percent and banks’ deposits - 0.2 percent). The biggest impact on the increase of deposits was the increase of legal entities’ deposits by MDL 3.1 billion (18.3 percent). Also, the individuals’ deposits increased by MDL 2.0 billion (5.2 percent).

Also, the deposits in MDL continued to increase and during the year 2017 went up by MDL 4.9 billion (16.7 percent) up to MDL 34.3 billion, the increase being also recorded for the foreign currency deposits - by MDL 0.1 billion (0.4 percent) up to MDL 25.6 billion.

Compliance with prudential requirements

The banks continue to maintain the liquidity indicators at a high level. Thus, the long-term liquidity indicator value (principle I of liquidity) accounted for 0.6 (limit ≤1), being at the same level recorded at the end of 2016. Current liquidity for the sector (principle II of liquidity) increased by 6.1 p.p., representing 55.4 percent (limit ≥20 percent), so more than half of the banking sector assets are concentrated in liquid assets. It is worth mentioning that the largest increase in the structure of liquid assets is held by deposits at the NBM - by 36.1 percent, liquid securities – 34.3 percent and net interbank resources - 20.3 percent. During the year 2017, the balance of these items increased by 11.5 percent, 35.7 percent and 30.7 percent respectively.

High level of risk-weighted capital adequacy ratio (average per sector - 31.0 percent, regulated limit for each bank ≥16 percent) allowed banks to absorb losses related to worsening of loan quality. At the same time, all banks comply with the regulated limit, which varies from 24.7 percent to 98.1 percent.

As of 31.12.2017, the Tier one capital amounted to MDL 10.1 billion and during the mentioned period it recorded an increase of 8.7 percent (MDL 812.5 million). The increase of the Tier I capital was mainly determined by obtaining the profit of MDL 1.5 billion. Most banks recovered the profit on capital strengthening, except for three banks that paid a dividend in the total amount of MDL 354.5 million. At the same time, the following factors influenced negatively the capital: the increase of the calculated amount but unreserved of allowances for impairment losses on asset and contingent liabilities by MDL 132.9 million, the formation by a bank of additional depreciation on assets in the amount of MDL 191.9 million, following the inspections of the external audit and of the NBM.

Regarding the Regulation on “large” exposures it should be specified that one bank is still violating the 15 percent prudential limit established by the NBM of total normative capital. However, this bank has a plan of reduction of exposure, complying to deadlines set out in the plan.

Compliance of the three largest banks to the Regulation on bank's related parties was verified by an international audit company and soon the NBM will take a decision regarding transactions with the related parties at these banks. For the banks that are not part of foreign financial groups, related parties were checked during on-site inspections and for the other banks they will be verified during the first half of 2018.

Income and profitability

On 31.12.2017, the profit amounted MDL 1.5 billion and in comparison with the similar period of the previous year it increased by 8.6 percent.

The Profit increase is determined by the increase of non-interest income by 6.8 percent and the decrease of the non-interest expenses by 7.6 percent. The income from taxes and fees represents a significant share in non-interest income - 61.7 percent, which increased compared to 31.12.2016 by 10.8 percent as a result of the increase in the number and volume of transactions performed through SAPI, SWIFT payment systems, as well as in the number and volume of card transactions issued in Moldova. On 31.12.2017, net income from taxes and fees amounted MDL 1.1 billion and registered an increase of 8.5 percent during the period of 31.12.2016 – 31.12.2017.

At the same time, the interest expenses (from deposits) decreased by 37.1 percent or MDL 1.1 billion. Interest income amounted MDL 4.7 billion, decreasing by MDL 1.5 billion compared to the similar period of the precedent year. It was generated, in particular, by loans and debts (MDL 3.8 billion).

On 31.12.2017, return on assets and return on equity recorded 1.8 percent and 11.1 percent respectively, being at the same level as in the precedent year.

On January 01, 2018, the law no. 202 on banks’ activity from October 06, 2017 entered into force. The Law on banks’ activity will strengthen the banking regulatory and supervision framework by aligning to European standards (transition from Basel I to Basel III).

Once the new law regulating the activity of banks in the Republic of Moldova entered into effect, there will undergo public consultations in stages the draft secondary regulatory framework subordinated to it (approximately 30 regulations), as well as the COREP reporting framework, which will enter into force at different time periods till 2020. Development of the mentioned regulations was initiated within the framework of the Twinning project of the European Union in order to strengthen the capacity of the NBM in the field of banking regulation and supervision in cooperation with the Central Bank of the Netherlands and the Central Bank of Romania.

It should be noted that the new regulatory framework will keep some previously applicable prudential provisions and will focus, predominantly, on strengthening the internal corporate governance and risk management practices in banks. New approaches were also introduced for the calculation of regulatory capital (own funds), risk-weighted capital adequacy (which will include, besides the credit risk other risks - operational, market and other risks related to banking activity) and liquidity ratios. In addition, new concepts will be introduced such as leverage ratio and risk associated to it, capital buffers, the internal capital adequacy assessment process (ICAAP) and the internal liquidity adequacy assessment process (ILAAP), disclosure requirements.

By the implementation of the law on banks’ activity, the National Bank of Moldova initiated the fundamental review of the banking supervision system, using the supervisor’s arguments based on risk, provisioning and approach of the supervision review and assessment process (SREP). Presently, the NBM possess a range of tools in order to apply the supervisory and remedial measures. Prudential supervision will be carried out including on a consolidated basis and on tight cooperation with foreign supervisors (including participation in supervision panels) and other competent authorities.

In order to improve the corporate governance in banks, on July 1, 2017, the Regulation on Internal Governance and Risk Management in Banks entered into force, with provisions concerning the risk management, requirements on policies for risk management and limits on risk appetite and risk profile, which ensure a gradual transition to the transposition package of the Basel III framework. In the near future, the specified regulation will be updated, that will strengthen the regulatory framework for issues related to the responsibilities of the management organ and its organization, the capital adequacy risk assessment (ICAAP) process and respectively the supervision and assessment process (SREP) etc.

Alignment of banking legislation of the Republic of Moldova to international standards by improving the quantitative and qualitative bank management mechanisms will contribute to promoting a secure and sound banking sector, to transparency increase, to confidence and attractiveness of the domestic banking sector for potential investors and creditors of banks, among whom are and the depositors, etc. The new framework conditions the development of new financial products and services due to ensuring a financial stability environment that permits maintaining financial soundness of banks and of the entire system.