Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova supervises the payment system of the Republic of Moldova and promotes a stable and efficient functioning of the automated inter-bank payment system

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

Note: The translation is unofficial, for information purpose only

Published in the Official Monitor of the Republic of Moldova, no. 183-194 of June 08, 2018, art. 904

Registered

by the Ministry of Justice

of the Republic of Moldova

under no.1336 of 4 June 2018

EXECUTIVE BOARD

OF THE NATIONAL BANK OF MOLDOVA

DECISION no.114

of 24 May 2018

on the approval of the Regulation on the treatment of the market risk

according to the standardised approach

(in force since 30 July 2018)

Pursuant to Art. 5 par. (1) letter d), Art. 11 par. (1), Art. 27 par. (1) letter c), Art.44 letter a) of the Law no.548-XIII of July 21, 1995 on the National Bank of Moldova (republished in the Official Monitor of the Republic of Moldova, 2015, no.297-300, Art. 544), with subsequent amendments and completions, Art. 60 and 71 of the Law no.202 of 6 October 2017 on the Bank`s activity (Official Monitor of the Republic of Moldova, 2017, no. 434-439, Art.727), with subsequent amendments and completions, the Executive Board of the National Bank of Moldova

RESOLVES:

1. To approve the Regulation on the treatment of the market risk according to the standardised approach, as laid down in the Annex hereto.

2. The Regulation referred to in paragraph 1 of this decision shall enter into force on 30 July 2018.

3. From the date of entry into force of the Regulation referred to in paragraph 1 of this decision, banks will ensure full compliance of their businesses, including internal policies and regulations, with its provisions.

Chairman

of the Executive Board

Sergiu CIOCLEA

Annex

to the Decision of the Executive Board

of the National Bank of Moldova

no. 114 of 24 May 2018

Regulation on the treatment of the market risk according to the standardised approach

This regulation transposes the following acts of the European Union:

Art.4 par. (1) sub-par. 50, 68, 69, 70, 72, 84, 85, 86, 87, 92, 96, 97, Art.102, Art.103, Art.104, Art.105 par.(1)-(13), Art.106, Art.325-327, Art.328 par.(1), Art.329 par.(1) and (2), Art. 330-335, Art.336 par.(1) and (4), Art.338-351, Art.352 par.(1)-(5), Art.353 par.(1) and (2), Art.354 par.(1), (2), (4) and (5), Art.355-357, Art.358 par.(1)-(3) and (5), Art.359-361 and Annex II of the Regulation No.575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No.648/2012, as amended by Commission Delegated Regulation (EU) No.2015/62 of 10 October 2014;

Commission Implementing Regulation (EU) No. 945/2014 of 4 September 2014 laying down implementing technical standards on relevant appropriately diversified indices according to Regulation (EU) No 575/2013 of the European Parliament and of the Council;

Commission Delegated Regulation (EU) No 525/2014 of 12 March 2014 supplementing Regulation (EU) No 575/2013 of the European Parliament and of the Council with regard to regulatory technical standards for the definition of market;

Commission Delegated Regulation (EU) No 528/2014 of 12 March 2014 supplementing Regulation (EU) No 575/2013 of the European Parliament and of the Council with regard to regulatory technical standards for non-delta risk of options in the standardised market risk approach;

Commission Implementing Regulation (EU) 2015/2197 of 27 November 2015 laying down implementing technical standards with regard to closely correlated currencies in accordance with Regulation (EU) No 575/2013 of the European Parliament and of the Council.

CHAPTER I

GENERAL PROVISIONS

Section 1

Subject matter and scope

1. This Regulation lays down the rules on own funds requirements for market risk according to the standardised approach for the purpose of calculating own funds requirements in accordance with the regulatory acts of the National Bank of Moldova on own funds and capital requirements.

2. This Regulation shall apply to banks, which are legal persons of the Republic of Moldova, as well as to branches of foreign banks established in the Republic of Moldova (hereinafter referred to as banks).

3. This Regulation shall apply on individual and, where appropriate, consolidated basis.

4. Subject to Item 5 and only for the purpose of calculating net positions and own funds requirements on a consolidated basis in accordance with this Regulation, banks may use positions in one bank to offset positions in another bank.

5. Banks may apply the provisions of Item 4 only subject to the permission of the National Bank of Moldova, which shall be granted if all of the following conditions are met:

a) there is a satisfactory allocation of own funds within the group;

b) the regulatory, legal or contractual framework in which the banks operate is such as to guarantee mutual financial support within the group.

6. Where there are undertakings located in third countries all of the following conditions shall be met in addition to those laid down in Item 5:

a) such undertakings have been authorised in a third country and satisfy the definition of a credit institution, recognized by other countries;

b) such undertakings comply, on an individual basis, with own funds requirements equivalent to those laid down in this Regulation and regulatory acts of the National Bank of Moldova;

c) no regulations exist in the concerned countries which might significantly affect the transfer of funds within the group.

Section 2

Definitions

7. The terms, concepts and expressions used in this Regulation have the meaning provided in the Law no. 202 of 6 October 2017 on the Bank’s Activity (hereinafter - Law no. 202 of October 6, 2017) and in the regulatory acts of the National Bank of Moldova issued in application of that law.

8. For the purposes of this Regulation, the terms and expressions below shall have the following meanings:

1) internal hedge shall mean a position that materially offsets the component risk elements between a trading book and a non-trading book position or sets of positions;

2) simple repurchase agreement shall mean a repurchase transaction of a single asset, or of similar, non-complex assets, as opposed to a basket of assets;

3) recognised exchange shall mean an exchange which meets all of the following conditions:

a) it is a regulated market, as defined in par. (10) of this Item;

b) it has a clearing mechanism whereby contracts listed in Annex 1 hereto are subject to daily margin requirements which, in the opinion of the competent authorities, provide appropriate protection.

4) delta shall represent the expected price variation of an option in relation to a variation in the price of the underlying instrument of the option.

5) stock financing shall mean positions where physical stock has been sold forward, whereas the cost of funding has been locked in until the date of the forward sale;

6) financial instrument shall mean any of the following:

a) any contract that gives rise to both a financial asset of one party and a financial liability or equity instrument of another party;

b) an instrument specified in Article 4 of the Law no. 171 of 11.07.2012 on the Capital market;

c) a derivative financial instrument;

d) a primary financial instrument;

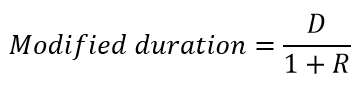

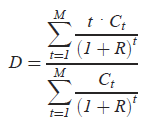

e) a cash instrument.

The instruments referred to in letters (a), (b) and (c) are only financial instruments if their value is derived from the price of an underlying financial instrument or another underlying item, a rate, or an index.

7) marking to model shall mean any valuation which has to be benchmarked, extrapolated or otherwise calculated from one or more market inputs;

8) marking to market shall mean the valuation of positions at readily available close out prices that are sourced independently, including exchange prices, screen prices or quotes from several independent reputable brokers;

9) reference obligation shall mean an obligation used for the purposes of determining the cash settlement value of a credit derivative;

10) regulated market shall mean a regulated market as defined by the Law no. 171 of 11.07.2012 on the Capital market;

11) trading book shall mean all positions in financial instruments and commodities held by a bank either with trading intent, or in order to hedge positions held with trading intent;

12) positions held with trading intent shall mean any of the following:

a) proprietary positions and positions arising from client servicing and market making;

b) positions intended to be resold short term;

c) positions intended to benefit from actual or expected short-term price differences between buying and selling prices or from other price or interest rate variations;

13) multilateral trading facility shall mean multilateral trading facility as defined in the Law no. 171 of 11.07.2012 on the Capital market;

14) convertible security shall mean a security which can be converted into another security, usually at the holder’s choice;

15) independent price verification shall mean a process by which market prices or marking to model inputs are regularly verified for accuracy and independence;

16) warrant shall mean a security that entitles the holder to purchase an underlying asset at a fixed price until or at the expiration date of the warrant and which can be settled by delivering the underlying asset or in cash.

CHAPTER II

TRADING BOOK

Section 1

Requirements for the trading book

9. A bank's trading book comprises all positions in financial instruments and commodities that are held either with trading intent or in order to hedge other items in the trading book, and which are either free of any restrictive clauses regarding their ability to be traded, or may be hedged.

10. Trading intent shall be evidenced on the basis of the strategies, policies and procedures set up by the bank to manage the positions or portfolio in accordance with Section 2 of this Chapter.

11. Banks shall establish and maintain systems and controls to manage their trading book in accordance with the Regulation on banks’ activity framework (approved by the decision of the Executive Board of the NBM no.146 of 07.06.2017).

12. Banks may include internal hedges in the calculation of capital requirements for the position risk provided that they are held with trading intent and that the requirements of Sections 2-5 of this Chapter are met.

Section 2

Management of the trading book

13. In managing its positions or sets of positions in the trading book a bank shall comply with all of the following requirements:

1) a bank shall have in place a clearly documented trading strategy for the position/instrument or portfolios, approved by the bank’s executive body, which shall include the expected holding period;

2) a bank shall have in place clearly defined policies and procedures for the active management of positions entered into on a trading desk. Those policies and procedures shall include the following:

a) which positions may be entered into by which trading desk;

b) position limits are set and monitored for appropriateness;

c) dealers have the autonomy to enter into and manage the position within agreed limits and according to the approved strategy;

d) positions are reported to the executive body as an integral part of the bank's risk management process;

e) positions are actively monitored with reference to market information sources and an assessment made of the marketability or hedgeability of the position or its component risks, including the assessment of the quality and availability of market inputs to the valuation process, level of market turnover, sizes of positions traded in the market;

f) active anti-fraud procedures and controls;

3) a bank shall have in place clearly defined policies and procedures to monitor the positions against the bank's trading strategy, including the monitoring of turnover and positions for which the originally intended holding period has been exceeded.

Section 3

Inclusion in the trading book

14. Banks shall have in place clearly defined policies and procedures for determining which position to include in the trading book for the purposes of calculating their capital requirements, in accordance with the requirements set out in Section 1 of this Chapter and the definition of trading book in accordance with par.(11) of Item 8, taking into account a bank's risk management capabilities and practices. A bank shall fully document its compliance with these policies and procedures and shall subject them to periodic internal audit.

15. Banks shall have in place clearly defined policies and procedures for the overall management of the trading book. These policies and procedures shall at least address:

1) the activities the bank considers to be trading and as constituting part of the trading book for own funds requirement purposes;

2) the extent to which a position can be marked-to-market daily by reference to an active, liquid two-way market;

3) for positions that are marked-to-model, the extent to which the bank can:

a) identify all material risks of the position;

b) hedge all material risks of the position with instruments for which an active, liquid two-way market exists;

c) derive reliable estimates for the key assumptions and parameters used in the model;

4) the extent to which a bank can, and is required to, generate valuations for the position that can be validated externally in a consistent manner;

5) the extent to which legal restrictions or other operational requirements would impede a bank's ability to effect a liquidation or hedge of the position in the short term;

6) the extent to which a bank can, and is required to, actively manage the risks of positions within its trading operation;

7) the extent to which the bank may transfer risk or positions between the non-trading and trading books and the criteria for such transfers.

Section 4

Requirements for prudent valuation

16. All trading book positions shall be subject to the standards for prudent valuation specified in this Section. Banks shall in particular ensure that the prudent valuation of their trading book positions achieves an appropriate degree of certainty having regard to the dynamic nature of trading book positions, the demands of prudential soundness and the mode of operation and purpose of capital requirements in respect of trading book positions.

17. Banks shall establish and maintain systems and controls sufficient to provide prudent and reliable valuation estimates. Those systems and controls shall include at least the following elements:

1) documented policies and procedures for the process of valuation, including clearly defined responsibilities of the various areas involved in the determination of the valuation, sources of market information and review of their appropriateness, guidelines for the use of unobservable inputs reflecting the bank's assumptions of what market participants would use in pricing the position, frequency of independent valuation, timing of closing prices, procedures for adjusting valuations, the month-end and ad-hoc verification procedures;

2) reporting lines for the department accountable for the valuation process that are clear and independent of the front office, which shall ultimately be to the management body.

18. Banks shall revalue trading book positions at least daily.

19. Banks shall mark their positions to market whenever possible, including when applying trading book capital treatment.

20. When marking to market, a bank shall use the more prudent side of bid and offer unless it can close out at mid market. Where banks make use of this derogation, they shall every six months inform the National Bank of Moldova of the positions concerned and furnish evidence that they can close out at mid-market.

21. Where marking to market is not possible, banks shall conservatively mark to model their positions and portfolios, including when calculating own funds requirements for positions in the trading book.

22. Banks shall comply with the following requirements when marking to model:

a) the executive body shall be aware of the elements of the trading book or of other fair-valued positions which are subject to mark to model and shall understand the materiality of the uncertainty thereby created in the reporting of the risk/performance of the business;

b) banks shall source market inputs, where possible, in line with market prices, and shall assess the appropriateness of the market inputs of the particular position being valued and the parameters of the model on a frequent basis;

c) where available, banks shall use valuation methodologies which are accepted market practice for particular financial instruments or commodities;

d) where the model is developed by the institution itself, it shall be based on appropriate assumptions, which have been assessed and challenged by suitably qualified parties independent of the development process;

e) banks shall have in place formal change control procedures and shall hold a secure copy of the model and use it periodically to check valuations;

f) the risk management unit shall be aware of the weaknesses of the models used and how best to reflect those in the valuation output;

g) banks' models shall be subject to periodic review to determine the accuracy of their performance, which shall include assessing the continued appropriateness of assumptions, analysis of profit and loss versus risk factors, and comparison of actual close out values to model outputs.

23. For the purposes ofletter (d) of Item 22, the model shall be developed or approved independently of the trading desk and shall be independently tested, including validation of the mathematics, assumptions and software implementation

24. Banks shall perform independent price verification in addition to daily marking to market or marking to model. Verification of market prices and model inputs shall be performed by a person or unit independent from persons or units that benefit from the trading book, at least monthly, or more frequently depending on the nature of the market or trading activity. Where independent pricing sources are not available or pricing sources are more subjective, prudent measures such as valuation adjustments may be appropriate.

25. Banks shall establish and maintain procedures for considering valuation adjustments.

26. Banks shall formally consider the following valuation adjustments: unearned credit spreads, close-out costs, operational risks, market price uncertainty, early termination, investing and funding costs, future administrative costs and, where relevant, model risk.

27. Banks shall establish and maintain procedures for calculating an adjustment to the current valuation of any less liquid positions, which can in particular arise from market events or bank-related situations, such as concentrated positions and/or positions for which the originally intended holding period has been exceeded. Banks shall, where necessary, make such adjustments in addition to any changes to the value of the position required for financial reporting purposes and shall design such adjustments to reflect the illiquidity of the position.

28. Under procedures laid down in Item 27, banks shall consider several factors when determining whether a valuation adjustment is necessary for less liquid positions. Those factors include the following:

a) the amount of time it would take to hedge out the position or the risks within the position;

b) the volatility and average of bid/offer spreads;

c) the availability of market quotes (number and identity of market makers) and the volatility and average of trading volumes including trading volumes during periods of market stress;

d) market concentrations;

e) the ageing of positions;

f) the extent to which valuation relies on marking-to-model;

g) the impact of other model risks.

29. When using third party valuations or marking to model, banks shall consider whether to apply a valuation adjustment. In addition, banks shall consider the need to establish adjustments for less liquid positions and on an ongoing basis review their continued suitability.

30. For the purposes of Item 29, banks shall also explicitly assess the need for valuation adjustments relating to the uncertainty of parameter inputs used by models.

31. With regard to complex products, including “n-th-to-default” credit derivatives, banks shall explicitly assess the need for valuation adjustments to reflect the model risk associated with using a possibly incorrect valuation methodology and the model risk associated with using unobservable (and possibly incorrect) calibration parameters in the valuation model.

Section 5

Internal hedges

32. An internal hedge shall in particular meet the following requirements:

a) it shall not be primarily intended to avoid or reduce own funds requirements;

b) it shall be properly documented and subject to particular internal approval and audit procedures;

c) it shall be dealt with at market conditions;

d) the market risk that is generated by the internal hedge shall be dynamically managed in the trading book within the authorised limits;

e) it shall be carefully monitored in accordance with adequate procedures.

33. The requirements of Item 32 shall apply without prejudice to the requirements applicable to the hedged position in the non-trading book.

34. By way of derogation from Items 32 and 33, when a bank hedges a non-trading book credit risk exposure or counterparty risk exposure using a credit derivative booked in its trading book using an internal hedge, the non-trading book exposure or counterparty risk exposure shall not be deemed to be hedged for the purposes of calculating risk-weighted exposure amounts unless the bank purchases from an eligible third party protection provider a corresponding credit derivative meeting the requirements for unfunded credit protection in the non-trading book.

CHAPTER III

Own funds requirements for position risk

Section 1

General provisions and specific instruments

35. A bank's own funds requirement for position risk shall be the sum of the own funds requirements for the general and specific risk of its positions in debt and equity instruments.

36. The absolute value of the excess of a bank's long (short) positions over its short (long) positions in the same equity, debt and convertible issues and identical financial futures, options, warrants and covered warrants shall be its net position in each of those different instruments. In calculating the net position, positions in derivative instruments shall be treated as laid down in Items 39-44. Banks' holdings of their own debt instruments shall be disregarded in calculating specific risk capital requirements under Items 58-60.

37. No netting shall be allowed between a convertible and an offsetting position in the instrument underlying it.

38. All net positions, irrespective of their signs, shall be converted on a daily basis into the bank's reporting currency at the exchange rate of the Moldovan leu set for the respective date, before their aggregation.

39. Interest-rate futures, forward-rate agreements (FRAs) and forward commitments to buy or sell debt instruments shall be treated as combinations of long and short positions. Thus a long interest-rate futures position shall be treated as a combination of a borrowing maturing on the delivery date of the futures contract and a holding of an asset with maturity date equal to that of the instrument or notional position underlying the futures contract in question. Similarly a sold FRA will be treated as a long position with a maturity date equal to the settlement date plus the contract period, and a short position with maturity equal to the settlement date. Both the borrowing and the asset holding shall be included in the first category set out in Table 2 in Item 58 in order to calculate the own funds requirement for specific risk for interest-rate futures and FRAs. A forward commitment to buy a debt instrument shall be treated as a combination of a borrowing maturing on the delivery date and a long (spot) position in the debt instrument itself. The borrowing shall be included in the first category set out in Table 2 in Item 58 for the purposes of specific risk, and the debt instrument under whichever column is appropriate for it in the same table.

40. For the purposes of Item 39, “long position” shall mean a position in which a bank has fixed the interest rate it will receive at some time in the future, and “short position” shall mean a position in which it has fixed the interest rate it will pay at some time in the future.

41. For the purposes of this Item, options and warrants on interest rates, debt instruments, equities, equity indices, financial futures, swaps and foreign currencies shall be treated as if they were positions equal in value to the amount of the underlying instrument to which the option refers, multiplied by its delta. The latter positions may be netted off against any offsetting positions in the identical underlying securities or derivatives. The delta used shall be that of the exchange concerned. For OTC-options, or where delta is not available from the exchange concerned, the institution may calculate delta itself using an appropriate model, subject to permission by the National Bank of Moldova. Permission shall be granted if the model appropriately estimates the rate of change of the option's or warrant's value with respect to small changes in the market price of the underlying.

42. Banks shall adequately reflect other risks, apart from the delta risk, associated with options in the own funds requirements under Item 43.

43. In compliance with provisions of Items 42, 120 and 147 of this Regulation, banks shall calculate their own funds requirements for the market risk, other than the delta risk, associated with options or warrants in accordance with one of the following approaches:

a) the simplified approach as set out in Annex 2, Section A to this Regulation;

b) the delta plus approach as set out in Annex 2, Section B to this Regulation;

c) the scenario approach as set out in Annex 2, Section C to this Regulation;

44. Swaps shall be treated for interest-rate risk purposes on the same basis as on-balance-sheet instruments. Thus, an interest-rate swap under which a bank receives floating-rate interest and pays fixed-rate interest shall be treated as equivalent to a long position in a floating-rate instrument of maturity equivalent to the period until the next interest fixing and a short position in a fixed-rate instrument with the same maturity as the swap itself.

45. Banks which mark to market and manage the interest-rate risk on the derivative instruments covered in Items 39-44 on a discounted-cash-flow basis may, subject to permission by the National Bank of Moldova, use sensitivity models to calculate the positions referred to in those Items and may use them for any bond which is amortised over its residual life rather than via one final repayment of principal.

46. Permission shall be granted if these models generate positions which have the same sensitivity to interest-rate changes as the underlying cash flows. This sensitivity shall be assessed with reference to independent movements in sample rates across the yield curve, with at least one sensitivity point in each of the maturity bands set out in Table 2 in Item 58. The positions shall be included in the calculation of own funds requirements for general risk of debt instruments.

47. Banks which do not use models under Item 45 may treat as fully offsetting any positions in derivative instruments covered in Items 39-44 which meet at least the following conditions:

1) the positions are of the same value and denominated in the same currency;

2) the reference rate (for floating-rate positions) or coupon (for fixed- rate positions) is closely matched;

3) the next interest-fixing date or, for fixed coupon positions, residual maturity corresponds with the following limits:

a) less than one month hence: same day;

b) between one month and one year hence: within seven days;

c) over one year hence: within 30 days.

48. When calculating the own funds requirement for general and specific risk of the party who assumes the credit risk (the ‘protection seller’), unless specified differently, the notional amount of the credit derivative contract shall be used.

49. Notwithstanding Item 48, a bank may elect to replace the notional value by the notional value plus the net market value change of the credit derivative since trade inception, a net downward change from the protection seller's perspective carrying a negative sign. For the purpose of calculating the specific risk charge, other than for total return swaps, the maturity of the credit derivative contract, rather than the maturity of the obligation, shall apply. Positions are determined as follows:

a) a total return swap creates a long position in the general risk of the reference obligation and a short position in the general risk of a government bond with a maturity equivalent to the period until the next interest fixing and which is assigned a 0% risk weight under the Regulation on the treatment of banks’ credit risk according to the standardised approach (approved by the decision no. 111 of 24.05.2018 of the Executive Board of the NBM.) It also creates a long position in the specific risk of the reference obligation;

b) a credit default swap does not create a position for general risk. For the purposes of specific risk, a bank shall record a synthetic long position in an obligation of the reference entity, unless the derivative is rated externally and meets the conditions for a qualifying debt item, in which case a long position in the derivative is recorded. If premium or interest payments are due under the product, these cash flows shall be represented as notional positions in government bonds;

c) a single name credit linked note creates a long position in the general risk of the note itself, as an interest rate product. For the purpose of specific risk, a synthetic long position is created in an obligation of the reference entity. An additional long position is created in the issuer of the note. Where the credit linked note has an external rating and meets the conditions for a qualifying debt item, a single long position with the specific risk of the note need only be recorded;

d) in addition to a long position in the specific risk of the issuer of the note, a multiple name credit linked note providing proportional protection creates a position in each reference entity, with the total notional amount of the contract assigned across the positions according to the proportion of the total notional amount that each exposure to a reference entity represents. Where more than one obligation of a reference entity can be selected, the obligation with the highest risk weighting determines the specific risk;

e) a “first-asset-to-default” credit derivative creates a position for the notional amount in an obligation of each reference entity. If the size of the maximum credit event payment is lower than the own funds requirement under the method in the first sentence of this point, the maximum payment amount may be taken as the own funds requirement for specific risk.

50. An “n-th-asset-to-default” credit derivative creates a position for the notional amount in an obligation of each reference entity less the n-1 reference entities with the lowest specific risk own funds requirement. If the size of the maximum credit event payment is lower than the own funds requirement under the method in the first sentence of this point, this amount may be taken as the own funds requirement for specific risk.

51. Where an “n-th-to-default” credit derivative is externally rated, the protection seller shall calculate the specific risk own funds requirement using the rating of the derivative and apply the respective securitisation risk weights according to Table 1.

Table 1

|

Credit quality step |

1 |

2 |

3 |

4 (only for credit assessments other than short-term credit assessments) |

All other credit quality steps |

|

„N-th-asset-to-default” credit derivatives positions |

20% |

50% |

100% |

350% |

1000% |

52. For the party who transfers credit risk (the protection buyer), the positions are determined as the mirror principle of the protection seller, with the exception of a credit linked note (which entails no short position in the issuer). When calculating the own funds requirement for the ‘protection buyer’, the notional amount of the credit derivative contract shall be used.

53. Notwithstanding the provisions of Item 52, a bank may elect to replace the notional value by the notional value plus the net market value change of the credit derivative since trade inception, a net downward change from the protection seller's perspective carrying a negative sign. If at a given moment there is a call option in combination with a step-up, such moment is treated as the maturity of the protection.

54. Credit derivatives in accordance with Item 62 or Item 64 shall be included only in the determination of the specific risk own funds requirement in accordance with Item 65.

55. A bank that transfers securities or guaranteed rights relating to title to securities in a repurchase agreement or lends securities in a securities lending shall include these securities in the calculation of its own funds requirement under this Chapter provided that such securities are trading book positions.

Section 2

Debt securities

56. Net positions shall be classified according to the currency in which they are denominated and shall calculate the own funds requirement for general and specific risk in each individual currency separately.

Sub-section 1

Specific risk

57. A bank may cap the own funds requirement for specific risk of a net position in a debt instrument at the maximum possible default-risk related loss. For a short position, that limit may be calculated as a change in value due to the instrument or, where relevant, the underlying names immediately becoming free of default risk.

58. A bank shall assign its net positions in the trading book, calculated in accordance with Items 36-38, to the appropriate categories in Table 2 on the basis of their issuer or obligor, external credit assessment, and residual maturity, and then multiply them by the weightings shown in that Table. It shall sum its weighted positions resulting from the application of this Item regardless of whether they are long or short in order to calculate its own funds requirement against specific risk.

Table 2

|

Categories |

Own funds requirements for specific risk |

|

Debt securities that would receive a 0 % risk weight under the Regulation on the treatment of banks’ credit risk according to the standardised approach. |

0% |

|

Debt securities that would receive a 20% or 50% risk weight under the Regulation on the treatment of banks’ credit risk according to the standardised approach, and other qualifying items as defined in Item 59. |

0,25% (residual term to final maturity six months or less) 1,00% (residual term to final maturity is greater than six months and up to and including 24 months ) 1,60% (residual term to final maturity is exceeding 24 months) |

|

Debt securities that would receive a 100% risk weight under the Regulation on the treatment of banks’ credit risk according to the standardised approach. |

8,00% |

|

Debt securities that would receive a 150% risk weight under the Regulation on the treatment of banks’ credit risk according to the standardised approach. |

12,00% |

59. Other qualifying items are:

1) long and short positions in assets for which a credit assessment by a nominated ECAI is not available and which meet all of the following conditions:

a) they are considered by the respective bank to be sufficiently liquid;

b) their investment quality is, according to the bank's own discretion, at least equivalent to that of the assets referred to under Table 2 second row;

c) they are listed on at least one regulated market in the Republic of Moldova or on a stock exchange in a third country provided that the exchange is recognised by the National Commission for Financial Market;

2) long and short positions in assets issued by the banks subject to the own funds requirements set out in the regulatory acts of the National Bank of Moldova, which are considered by the bank concerned to be sufficiently liquid and whose investment quality is, according to the bank's own discretion, at least equivalent to that of the assets referred to under Table 2 second row;

3) securities issued by a bank that are deemed to be of equivalent, or higher, credit quality than those associated with credit quality step 2 under the standardised approach for credit risk of exposures to banks and that are subject to supervisory and regulatory arrangements comparable to those set out in the regulatory acts of the National Bank of Moldova and in the Law no. 202 of 6 October 2017.

60. Banks that make use of Item 59 shall have a documented methodology in place to assess whether assets meet the requirements in those points and shall notify this methodology to the National Bank of Moldova.

61. The correlation trading portfolio shall consist of “n-th-to-default” credit derivatives where all reference instruments are either of the following:

a) single-name instruments, including single-name credit derivatives, for which a liquid two-way market exists;

b) commonly-traded indices based on the concerned reference entities.

62. For the purposes of Item 61, a two-way market is deemed to exist where there are independent bona fide offers to buy and sell so that a price reasonably related to the last sales price or current bona fide competitive bid and offer quotations can be determined within one day and settled at such price within a relatively short time conforming to trade custom.

63. Positions which reference any of the following shall not be part of the correlation trading portfolio:

a) an underlying that may be assigned to the exposure class of “retail exposures” or to the exposure class of “exposures secured by mortgages on immovable property” under the standardised approach for credit risk in a bank's non-trading book;

b) a claim on a special purpose entity, collateralised, directly or indirectly, by a position that would itself not be eligible for inclusion in the correlation trading portfolio in accordance with Items 61-63.

64. A bank may include in the correlation trading portfolio positions which are not “n-th-to-default” credit derivatives, but which hedge other positions of that portfolio, provided that a liquid two-way market as described in Item 62 exists for the concerned instrument or its underlyings.

65. A bank shall determine the larger of the following amounts as the specific risk own funds requirement for the correlation trading portfolio:

a) the total specific risk own funds requirement that would apply just to the net long positions of the correlation trading portfolio;

b) the total specific risk own funds requirement that would apply just to the net short positions of the correlation trading portfolio.

Sub-section 2

Maturity-based calculation of general risk

66. In order to calculate own funds requirements against general risk all positions shall be weighted according to maturity as explained in Item 67 in order to compute the amount of own funds required against them. This requirement shall be reduced when a weighted position is held alongside an opposite weighted position within the same maturity band. A reduction in the requirement shall also be made when the opposite weighted positions fall into different maturity bands, with the size of this reduction depending both on whether the two positions fall into the same zone, or not, and on the particular zones they fall into.

67. The bank shall assign its net positions to the appropriate maturity bands in column 2 or 3, as appropriate, in Table 3 in this Sub-section. The bank shall do so on the basis of residual maturity in the case of fixed-rate instruments and on the basis of the period until the interest rate is next set in the case of instruments on which the interest rate is variable before final maturity. The bank shall also distinguish between debt instruments with a coupon of 3% or more and those with a coupon of less than 3% and thus allocate them to column 2 or column 3 in the Table 3 below. It shall then multiply each of them by the weighing for the maturity band in question in column 4 in Table 3.

68. A bank shall then calculate the sum of the weighted long positions and the sum of the weighted short positions in each maturity band. The amount of the former which are matched by the latter in a given maturity band shall be the matched weighted position in that band, while the residual long or short position shall be the unmatched weighted position for the same band. The total of the matched weighted positions in all bands shall then be calculated.

69. A bank shall compute the totals of the unmatched weighted long positions for the bands included in each of the zones in Table 3 in order to derive the unmatched weighted long position for each zone. Similarly, the sum of the unmatched weighted short positions for each band in a particular zone shall be summed to compute the unmatched weighted short position for that zone. That part of the unmatched weighted long position for a given zone that is matched by the unmatched weighted short position for the same zone shall be the matched weighted position for that zone. That part of the unmatched weighted long or unmatched weighted short position for a zone that cannot be thus matched shall be the unmatched weighted position for that zone.

Table 3

|

Zone |

Maturity band |

weighting ( in %) |

Assumed interest rate change (in %) |

|

|

coupon of 3% or more |

coupon of less than 3% |

|||

|

One |

0 ≤ 1 month |

0 ≤ 1 month |

0.00 |

- |

|

> 1 ≤ 3 months |

> 1 ≤ 3 months |

0.20 |

1.00 |

|

|

> 3 ≤ 6 months |

> 3 ≤ 6 months |

0.40 |

1.00 |

|

|

> 6 ≤ 12 months |

> 6 ≤ 12 months |

0.70 |

1.00 |

|

|

Two |

> 1 ≤ 2 years |

> 1.0 ≤ 1.9 years |

1.25 |

0.90 |

|

> 2 ≤ 3 years |

> 1.9 ≤ 2.8 years |

1.75 |

0.80 |

|

|

> 3 ≤ 4 years |

> 2.8 ≤ 3.6 years |

2.25 |

0.75 |

|

|

Three |

> 4 ≤ 5 years |

> 3.6 ≤ 4.3 years |

2.75 |

0.75 |

|

> 5 ≤ 7 years |

> 4.3 ≤ 5.7 years |

3.25 |

0.70 |

|

|

> 7 ≤ 10 years |

> 5.7 ≤ 7.3 years |

3.75 |

0.65 |

|

|

> 10 ≤ 15 years |

> 7.3 ≤ 9.3 years |

4.50 |

0.60 |

|

|

> 15 ≤ 20 years |

> 9.3 ≤ 10.6 years |

5.25 |

0.60 |

|

|

> 20 years |

> 10.6 ≤ 12.0 years |

6.00 |

0.60 |

|

|

|

> 12.0 ≤ 20.0 years |

8.00 |

0.60 |

|

|

|

> 20 years |

12.50 |

0.60 |

|

70. The amount of the unmatched weighted long or short position in zone one which is matched by the unmatched weighted short or long position in zone two shall then be the matched weighted position between zones one and two. The same calculation shall then be undertaken with regard to that part of the unmatched weighted position in zone two which is left over and the unmatched weighted position in zone three in order to calculate the matched weighted position between zones two and three.

71. The bank may reverse the order laid down in Item 70 so as to calculate the matched weighted position between zones two and three before calculating that position between zones one and two.

72. The remainder of the unmatched weighted position in zone one shall then be matched with what remains of that for zone three after the latter's matching with zone two in order to derive the matched weighted position between zones one and three.

73. Residual positions, following the three separate matching calculations specified in Items 70-72 shall be summed.

74. The bank's own funds requirement shall be calculated as the sum of:

a) 10 % of the sum of the matched weighted positions in all maturity bands;

b) 40 % of the matched weighted position in zone one;

c) 30 % of the matched weighted position in zone two;

d) 30 % of the matched weighted position in zone three;

e) 40 % of the matched weighted position between zones one and two and between zones two and three;

f) 150 % of the matched weighted position between zones one and three;

g) 100 % of the residual unmatched weighted positions.

Sub-section 3

Duration-based calculation of general risk

75. Banks may use an approach for calculating the own funds requirement for the general risk on debt instruments which reflects duration, instead of the approach set out in Sub-section 2 of this Section, provided that the bank does so on a consistent basis.

76. Under the duration-based approach referred to in Item 75, the bank shall take the market value of each fixed-rate debt instrument and hence calculate its yield to maturity, which is implied discount rate for that instrument. In the case of floating-rate instruments, the bank shall take the market value of each instrument and hence calculate its yield on the assumption that the principal is due when the interest rate can next be changed.

77. The bank shall then calculate the modified duration of each debt instrument on the basis of the following formula:

where:

D = duration calculated according to the following formula:

where:

R = yield to maturity;

Ct = cash payment in time t;

M = total maturity.

Correction shall be made to the calculation of the modified duration for debt instruments which are subject to prepayment risk.

78. The bank shall then allocate each debt instrument to the appropriate zone in Table 4. It shall do so on the basis of the modified duration of each instrument.

Table 4

|

Zone |

Modified duration (in years) |

Assumed interest (change in %) |

|

One |

> 0 ≤ 1.0 |

1.0 |

|

Two |

> 1.0 ≤ 3.6 |

0.85 |

|

Three |

> 3.6 |

0.7 |

79. The bank shall then calculate the duration-weighted position for each instrument by multiplying its market price by its modified duration and by the assumed interest-rate change for an instrument with that particular modified duration (see column 3 in Table 4).

80. The bank shall calculate its duration-weighted long and its duration-weighted short positions within each zone. The amount of the former which are matched by the latter within each zone shall be the matched duration-weighted position for that zone.

81. The bank shall then calculate the unmatched duration-weighted positions for each zone. It shall then follow the procedures laid down for unmatched weighted positions in Items 70-73.

82. The bank's own funds requirement shall then be calculated as the sum of the following:

a) 2% of the matched duration-weighted position for each zone;

b) 40% of the matched duration-weighted positions between zones one and two and between zones two and three;

c) 150 % of the matched duration-weighted position between zones one and three;

d) 100 % of the residual unmatched duration-weighted positions.

Section 3

Equities

83. The bank shall separately sum all its net long positions and all its net short positions in accordance with Items 36-38. The sum of the absolute values of the two figures shall be its overall gross position.

84. The bank shall calculate, separately for each market, the difference between the sum of the net long and the net short positions. The sum of the absolute values of those differences shall be its overall net position.

85. For the purposes of Item 84, the term „market” shall mean:

a) for the euro area, all equities listed on stock exchanges in the Member States of the European Union that have adopted the euro as the national currency;

b) for other States, all equities listed on stock exchanges within a national jurisdiction.

86. The bank shall multiply its overall gross position by 8% in order to calculate its own funds requirement against specific risk.

87. The bank shall multiply its overall net position by 8% in order to calculate its own funds requirement against general risk.

88. Stock-index futures, the delta-weighted equivalents of options in stock-index futures and stock indices collectively referred to hereafter as ‘stock-index futures’, may be broken down into positions in each of their constituent equities. These positions may be treated as underlying positions in the equities in question, and may be netted against opposite positions in the underlying equities themselves. Banks shall notify the National Bank of Moldova of the use they make of that treatment.

89. Where a stock-index future is not broken down into its underlying positions, it shall be treated as if it were an individual equity.

90. For the purposes of Item 89, the specific risk on this individual equity can be ignored if the stock-index future in question is exchange traded and represents a relevant appropriately diversified index.

91. A list of stock indices for which the treatments specified under Item 90 are available is included in Annex 3 to this Regulation.

Section 4

Underwriting

92. In the case of the underwriting of debt and equity instruments, a bank may use the following procedure in calculating its own funds requirements. The bank shall first calculate the net positions by deducting the underwriting positions which are subscribed or sub-underwritten by third parties on the basis of formal agreements. The bank shall then reduce the net positions by the reduction factors listed in Table 5 and calculate its own funds requirements using the reduced underwriting positions.

Table 5

|

Working day 0; |

100% |

|

Working day 1; |

90% |

|

Working day 2-3; |

75% |

|

Working day 4; |

50% |

|

Working day 5; |

25% |

|

After working day 5; |

0% |

93. “Working day zero” shall be the working day on which a bank becomes unconditionally committed to accepting a known quantity of securities at an agreed price.

94. The bank shall notify to the National Bank of Moldova the use it makes of Items 92-93.

Section 5

Specific risk own funds requirements for positions hedged by credit derivatives

Sub-section 1

Allowance for hedges by credit derivatives

95. The National Bank of Moldova shall give allowance for hedges provided by credit derivatives, in accordance with the principles set out in Items 96-102.

96. Banks shall treat the position in the credit derivative as one ‘leg’ and the hedged position that has the same nominal, or, where applicable, notional amount, as the other ‘leg’.

97. Full allowance shall be given when the values of the two legs always move in the opposite direction and broadly to the same extent. This will be the case in the following situations:

a) the two legs consist of completely identical instruments;

b) a long cash position is hedged by a total rate of return swap (or vice versa) and there is an exact match between the reference obligation and the underlying exposure (i.e., the cash position). The maturity of the swap itself may be different from that of the underlying exposure.

98. In the situations referred to in Item 97, a specific risk own funds requirement shall not be applied to either side of the position.

99. An 80 % offset will be applied when the values of the two legs always move in the opposite direction and where there is an exact match in terms of the reference obligation, the maturity of both the reference obligation and the credit derivative, and the currency of the underlying exposure. In addition, key features of the credit derivative contract shall not cause the price movement of the credit derivative to materially deviate from the price movements of the cash position. To the extent that the transaction transfers risk, an 80% specific risk offset will be applied to the side of the transaction with the higher own funds requirement, while the specific risk requirements on the other side shall be zero.

100. Partial allowance shall be given, absentthe situations in Items 97-99, in the following situations:

1) the position falls under Item 97 letter b), but there is an asset mismatch between the reference obligation and the underlying exposure. However, the positions meet the following requirements:

a) the reference obligation ranks pari passu with or is junior to the underlying obligation;

b) the underlying obligation and reference obligation share the same obligor and have legally enforceable cross-default or cross-acceleration clauses;

2) the position falls under Item 97 letter a) or Item 99, but there is a currency or maturity mismatch between the credit protection and the underlying asset. Such currency mismatch shall be included in the own funds requirement for foreign exchange risk;

3) the position falls under Item 99, but there is an asset mismatch between the cash position and the credit derivative. However, the underlying asset is included in the (deliverable) obligations in the credit derivative documentation.

101. For the purposes of Item 100, in order to give partial allowance, rather than adding the specific risk own funds requirements for each side of the transaction, only the higher of the two own funds requirements shall apply.

102. In all situations not falling under Items 97-101, an own funds requirement for specific risk shall be calculated for both sides of the positions separately.

Sub-section 2

Allowance for hedges by firstand n-th-to-default credit derivatives

103. In the case of first-to-default credit derivatives and n-th-to-default credit derivatives, the following treatment applies for the allowance to be given in accordance with Sub-section 1 of Section 5:

a) where a bank obtains credit protection for a number of reference entities underlying a credit derivative under the terms that the first default among the assets shall trigger payment and that this credit event shall terminate the contract, the bank may offset specific risk for the reference entity to which the lowest specific risk percentage charge among the underlying reference entities applies in accordance with Table 2 in Item 58 of this Regulation;

b) where the nth default among the exposures triggers payment under the credit protection, the protection buyer may only offset specific risk if protection has also been obtained for defaults 1 to n-1 or when n-1 defaults have already occurred. In such cases, the methodology set out in letter a) for “first-to-default” credit derivatives shall be followed, appropriately amended for “nth-to-default” products.

Section 6

Own funds requirements for CIUs

Sub-section 1

Own funds requirements for CIUs

104. Without prejudice to other provisions in this Section, positions in CIUs shall be subject to an own funds requirement for position risk, comprising specific and general risk, of 32%.

105. Without prejudice to the provisions under Sub-section 2 of Section 1, Chapter IV, taken together with the amended gold treatment set out in Item 119, positions in CIUs shall be subject to an own funds requirement for position risk, comprising specific and general risk, and foreign-exchange risk of 40%.

106. Unless noted otherwise in Sub-section 3 of Section 6, no netting is permitted between the underlying investments of a CIU and other positions held by the bank.

Sub-section 2

General criteria for CIUs

107. CIUs shall be eligible for the approach set out in Sub-section 3 of this Section, where all the following conditions are met:

1) the CIU's prospectus or equivalent document shall include all of the following:

a) the categories of assets in which the CIU is authorised to invest;

b) where investment limits apply, the relative limits and the methodologies to calculate them;

c) where leverage is allowed, the maximum level of leverage;

d) where concluding OTC financial derivatives transactions or repurchase transactions or securities borrowing or lending is allowed, a policy to limit counterparty risk arising from these transactions;

2) the business of the CIU shall be reported in half-yearly and annual reports to enable an assessment to be made of the assets and liabilities, income and operations over the reporting period;

3) the shares or units of the CIU shall be redeemable in cash, out of the undertaking's assets, on a daily basis at the request of the unit holder;

4) investments in the CIU shall be segregated from the assets of the CIU manager;

5) there shall be adequate risk assessment of the CIU, by the investing bank;

6) CIUs shall be managed by persons supervised in accordance with the Law no. 171 of 11.07.2013 on Capital Market or equivalent legislation applicable in the origin state of the CIU.

Sub-section 3

Specific methods for CIUs

108. Where the bank is aware of the underlying investments of the CIU on a daily basis, the bank may look through to those underlying investments in order to calculate the own funds requirements for position risk, comprising specific and general risk. Under such an approach, positions in CIUs shall be treated as positions in the underlying investments of the CIU. Netting shall be permitted between positions in the underlying investments of the CIU and other positions held by the institution, provided that the bank holds a sufficient quantity of shares or units to allow for redemption/creation in exchange for the underlying investments.

109. Banks may calculate the own funds requirements for position risk, comprising specific and general risk, for positions in CIUs by assuming positions representing those necessary to replicate the composition and performance of the externally generated index or fixed basket of equities or debt securities referred to in lettera), subject to the following conditions:

a) the purpose of the CIU's mandate is to replicate the composition and performance of an externally generated index or fixed basket of equities or debt securities;

b) a minimum correlation coefficient between daily returns on the CIU and the index or basket of equities or debt securities it tracks of 0,9 can be clearly established over a minimum period of six months.

110. Where the bank is not aware of the underlying investments of the CIU on a daily basis, the bank may calculate the own funds requirements for position risk, comprising specific and general risk, subject to the following conditions:

a) it will be assumed that the CIU first invests to the maximum extent allowed under its mandate in the asset classes attracting the highest own funds requirement for specific and general risk separately, and then continues making investments in descending order until the maximum total investment limit is reached. The position in the CIU will be treated as a direct holding in the assumed position;

b) the bank shall take account of the maximum indirect exposure that it could achieve by taking leveraged positions through the CIU when calculating their own funds requirement for specific and general risk separately, by proportionally increasing the position in the CIU up to the maximum exposure to the underlying investment items resulting from the mandate;

c) if the own funds requirement for specific and general risk together in accordance with this item exceeds that set out in Items 104-105, the own funds requirement shall be capped at that level.

111. The bank may rely on the following third parties to calculate and report own funds requirements for position risk for positions in CIUs falling under this Item and Items 108-110, in accordance with the methods set out in this Chapter:

a) the depository of the CIU provided that the CIU exclusively invests in securities and deposits all securities at this depository;

The correctness of the calculation shall be confirmed by an external auditor.

CHAPTER IV

Own funds requirements for foreign-exchange risk

Section 1

De minimis andweighting for foreign-exchange risk

112. If the sum of a bank's overall net foreign-exchange position and its net gold position, calculated in accordance with the procedure set out in Sub-section 1 exceeds 2% of its total own funds, the bank shall calculate an own funds requirement for foreign-exchange risk. The own funds requirement for foreign-exchange risk shall be the sum of its overall net foreign-exchange position and its net gold position in the reporting currency, multiplied by 8%.

Sub-section 1

Calculation of the overall net foreign-exchange position

113. The bank's net open position in each currency (including the reporting currency) and in gold shall be calculated as the sum of the following elements (positive or negative):

a) the net spot position (i.e. all asset items less all liability items, including accrued interest, in the currency in question or, for gold, the net spot position in gold);

b) the net forward position, which are all amounts to be received less all amounts to be paid under forward exchange and gold transactions, including currency and gold futures and the principal on currency swaps not included in the spot position;

c) irrevocable guarantees and similar instruments that are certain to be called and likely to be irrecoverable;

d) the net delta, or delta-based, equivalent of the total book of foreign-currency and gold options;

e) the market value of other options.

114. The delta used for purposes of letter d) of Art. 113 shall be that of the exchange concerned. For OTC options, or where delta is not available from the exchange concerned, the bank may calculate delta itself using an appropriate model, subject to permission by the National Bank of Moldova. Permission shall be granted if the model appropriately estimates the rate of change of the option's or warrant's value with respect to small changes in the market price of the underlying.

115. The bank may include net future income/expenses not yet accrued but already fully hedged if it does so consistently.

116. The bank may break down net positions in composite currencies into the component currencies in accordance with the quotas in force.

117. Any positions which a bank has deliberately taken in order to hedge against the adverse effect of the exchange rate on its ratios in accordance with the provisions of the Regulation on own funds and capital requirements (approved by the decision of the Executive Board of the NBM no. 109 of 24.05.2018) may, subject to permission by the National Bank of Moldova, be excluded from the calculation of net open currency positions. Such positions shall be of a non-trading or structural nature and any variation of the terms of their exclusion, subject to separate permission by the National Bank of Moldova. The same treatment subject to the same conditions may be applied to positions which a bank has, which relate to items that are already deducted in the calculation of own funds.

118. A bank may use the net present value when calculating the net open position in each currency and in gold provided that the bank applies this approach consistently.

119. Net short and long positions in each currency other than the reporting currency and the net long or short position in gold shall be converted at spot rates into the reporting currency. They shall then be summed separately to form the total of the net short positions and the total of the net long positions, respectively. The higher of these two totals shall be the bank's overall net foreign-exchange position.

120. The bank shall adequately reflect other risks associated with options, apart from the delta risk, in the own funds requirements according to Item 43.

Sub-section 2

Foreign-exchange risk of CIUs

121. For the purposes of Sub-section 1 of this Section, in respect of CIUs the actual foreign exchange positions of the CIU shall be taken into account.

122. The bank may rely on the following third parties' reporting of the foreign exchange positions in the CIU:

a) the depository institution of the CIU provided that the CIU exclusively invests in securities and deposits all securities at this depository institution;

123. The correctness of the calculation shall be confirmed by an external auditor.

124. Where a bank is not aware of the foreign exchange positions in a CIU, it shall be assumed that the CIU has invested up to the maximum extent allowed under the CIU's mandate in foreign exchange and the bank shall, for trading book positions, take account of the maximum indirect exposure that it could achieve by taking leveraged positions through the CIU when calculating their own funds requirement for foreign-exchange risk.

125. For the purposes of Item 124, this shall be done by proportionally increasing the position in the CIU up to the maximum exposure to the underlying investment items resulting from the investment mandate. The assumed position of the CIU in foreign exchange shall be treated as a separate currency according to the treatment of investments in gold, subject to the addition of the total long position to the total long open foreign exchange position and the total short position to the total short open foreign exchange position where the direction of the CIU's investment is available.

126. Under Items 124-125, there shall be no netting allowed between such positions prior to the calculation.

Section 2

Closely correlated currencies

127. The bank may provide lower own funds requirements against positions in relevant closely correlated currencies.

128. For the purposes of this Section, a pair of currencies is deemed to be closely correlated only if the likelihood of a loss — calculated on the basis of daily exchange-rate data for the preceding three or five years — occurring on equal and opposite positions in such currencies over the following 10 working days, which is 4% or less of the value of the matched position in question (valued in terms of the reporting currency) has a probability of at least 99%, when an observation period of three years is used, and 95%, when an observation period of five years is used.

129. The own funds requirement on the matched position in two closely correlated currencies shall be 4% multiplied by the value of the matched position.

130. Pairs of currencies that meet the requirements of Items 127-129 are set out in Annex 4 to this Regulation.

131. In calculating the requirements of this Section, the bank may disregard positions in currencies, which are subject to a legally binding intergovernmental agreement to limit its variation relative to other currencies covered by the same agreement.

132. For the purposes of Item 131, the bank shall calculate its matched positions in such currencies and subject them to an own funds requirement no lower than half of the maximum permissible variation laid down in the intergovernmental agreement in question in respect of the currencies concerned.

133. The own funds requirement on the matched positions in currencies of the EU Member States participating in the second stage of the economic and monetary union may be calculated as 1,6% of the value of such matched positions.

134. Only the unmatched positions in currencies referred to in this Section shall be incorporated into the overall net open position in accordance with Item 119.

135. Where daily exchange-rate data for the preceding three or five years — occurring on equal and opposite positions in a pair of currencies over the following 10 working days show that these two currencies are perfectly positively correlated and the bank always can face a zero bid/ask spread on the respective trades, the bank can, upon explicit permission by the National Bank of Moldova, apply an own funds requirement of 0% up to and including the date of 31.12.2018.

CHAPTER V

Own funds requirements for commodities risk

Section 1

Businesses and positions exposed to commodities risk

136. Subject to Items 137-148, banks shall calculate the own funds requirement for commodities risk using one of the methods set out in Section 2, Sub-section 1-3 of this Chapter.

137. Banks which carry out activities with financial instruments with underilying agricultural raw materials and hold or take positions in these instruments may determine own funds requirements for their physical commodity stock at the end of each year for the following year where all of the following conditions are met:

a) at any time of the year a bank holds own funds for this risk which are not lower than the average own funds requirement for that risk estimated on a conservative basis for the coming year;

b) it estimates on a conservative basis the expected volatility for the figure calculated under letter a);

c) its average own funds requirement for this risk does not exceed 5% of its own funds or 10 million lei and, taking into account the volatility estimated in accordance with letter b), the expected peak own funds requirements do not exceed 6,5 % of its own funds;

d) the bank monitors on an ongoing basis whether the estimates carried out under letter a) and b) still reflect the reality.

138. The bank shall notify to the National Bank of Moldova the use it makes of the option provided in Item 137.

139. Each position in commodities or commodity derivatives shall be expressed in terms of the standard unit of measurement. The spot price in each commodity shall be expressed in the reporting currency.

140. Positions in gold or gold derivatives shall be considered as being subject to foreign-exchange risk and treated in accordance with own funds requirements for foreign-exchange risk under Chapter IV of this Regulation, for the purpose of calculating commodities risk.

141. For the purposes of Item 155, the excess of a bank's long positions over its short positions, or vice versa, in the same commodity and identical commodity futures, options and warrants shall be its net position in each commodity. Positions in derivative instruments shall be treated, as laid down in Items 143-148, as positions in the underlying commodity.

142. For the purposes of calculating a position in a commodity, the following positions shall be treated as positions in the same commodity:

a) positions in different sub-categories of commodities in cases where the sub-categories are deliverable against each other;

b) positions in similar commodities if they are close substitutes and where a minimum correlation of 0,9 between price movements can be clearly established over a minimum period of one year.

143. Commodity futures and forward commitments to buy or sell individual commodities shall be incorporated in the measurement system as notional amounts in terms of the standard unit of measurement and assigned a maturity with reference to expiry date.

144. Commodity swaps where one side of the transaction is a fixed price and the other the current market price shall be treated, as a series of positions equal to the notional amount of the contract, with, where relevant, one position corresponding with each payment on the swap and slotted into the maturity bands, as laid down in Item 149.

145. For the purposes of Item 144, the positions shall be long positions if the bank is paying a fixed price and receiving a floating price and short positions if the bank is receiving a fixed price and paying a floating price. Commodity swaps where the sides of the transaction are in different commodities are to be reported in the relevant reporting ladder for the maturity ladder approach.

146. For the purposes of this Chapter, options and warrants on commodities or on commodity derivatives shall be treated as if they were positions equal in value to the amount of the underlying to which the option refers, multiplied by its delta. The latter positions may be netted off against any offsetting positions in the identical underlying commodity or commodity derivative. The delta used shall be that of the exchange concerned. For OTC options, or where delta is not available from the exchange concerned the bank may calculate delta itself using an appropriate model, subject to permission by the National Bank of Moldova. Permission shall be granted if the model appropriately estimates the rate of change of the option's or warrant's value with respect to small changes in the market price of the underlying.

147. Banks shall adequately reflect other risks associated with options, apart from the delta risk, in the own funds requirements.

148. Where a bank is either of the following, it shall include the commodities concerned in the calculation of its own funds requirement for commodities risk:

a) the transferor of commodities or guaranteed rights relating to title to commodities in a repurchase agreement;

b) the lender of commodities in a commodities lending agreement.

Section 2

Approaches for calculating own funds requirements for commodities risk

Sub-section 1

Maturity ladder approach

149. The bank shall use a separate maturity ladder in line with Table 6 for each commodity. All positions in that commodity shall be assigned to the appropriate maturity bands. Physical stocks shall be assigned to the first maturity band between 0 and up to and including 1 month.

Table 6

|

Maturity band (1) |

Spread rate (in %) (2) |

|

0 ≤ 1 month |

1.50 |

|

> 1 ≤ 3 months |

1.50 |

|

> 3 ≤ 6 months |

1.50 |

|

> 6 ≤ 12 months |

1.50 |

|

> 1 ≤ 2 years |

1.50 |

|

> 2 ≤ 3 years |

1.50 |

|

> 3 years |

1.50 |

150. Positions in the same commodity may be offset and assigned to the appropriate maturity bands on a net basis for the following:

a) positions in contracts maturing on the same date;

b) positions in contracts maturing within 10 days of each other if the contracts are traded on markets which have daily delivery dates.

151. Having acomplished the requirements of Item 150, the bank shall calculate the sum of the long positions and the sum of the short positions in each maturity band. The amount of the former which are matched by the latter in a given maturity band shall be the matched positions in that band, while the residual long or short position shall be the unmatched position for the same band.

152. That part of the unmatched long position for a given maturity band that is matched by the unmatched short position, or vice versa, for a maturity band further out shall be the matched position between two maturity bands. That part of the unmatched long or unmatched short position that cannot be thus matched shall be the unmatched position.

153. The bank’s own funds requirement for each commodity shall be calculated on the basis of the relevant maturity ladder as the sum of the following:

a) the sum of the matched long and short positions, multiplied by the appropriate spread rate as indicated in the second column of Table 6 for each maturity band and by the spot price for the commodity;