Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

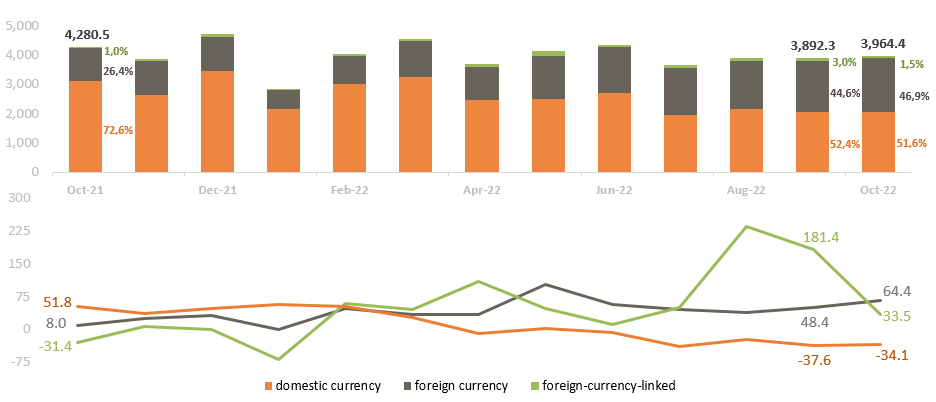

In October 2022, new loans extended1 by banks totaled MDL 3,964.4 million, decreasing by 7.4% compared to October 2021.

The structure of loans granted (Chart 1) in the reporting month evolved as follows:

Chart 1

Dynamics of new loans extended, million MDL (upper chart) and the annual growth rate of new loans extended by banks, % (lower chart)

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

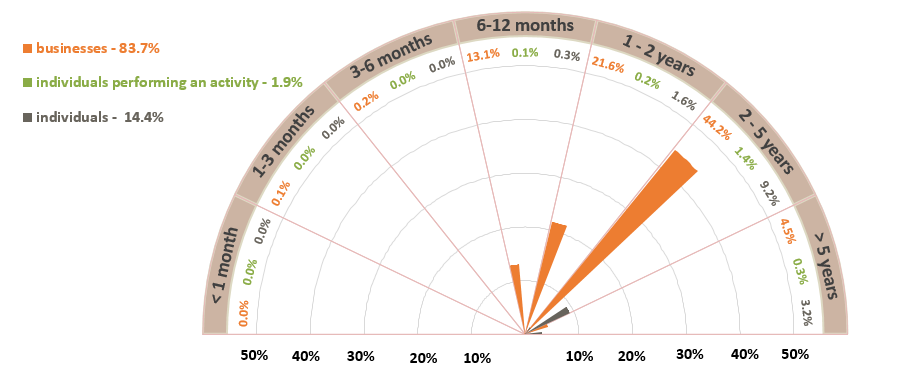

In terms of maturity (Chart 2), loans with maturity ranging from 2 to 5 years recorded the highest demand, with a share of 54.8%. The share of businesses’ loans with this term constituted 44.2% in the total amount of extended loans.

Chart 2

New loans extended by maturity and their structure, %

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

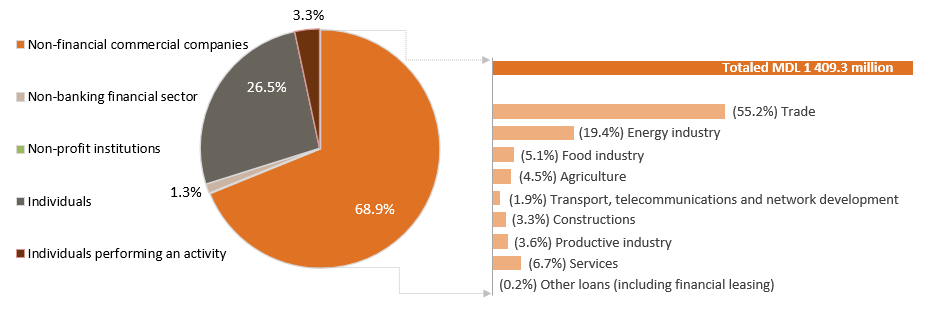

Domestic currency loans (Chart 3) were mainly represented by loans extended to non-financial commercial companies (68.9%) and to individuals (26.5%). Within loans to non-financial commercial companies, loans to trade dominated (55.2%).

Chart 3

Domestic currency loans by sectors, %

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

Foreign currency loans were mainly requested by non-financial commercial companies (95.6%), and the largest share (50.4%) belongs to trade.

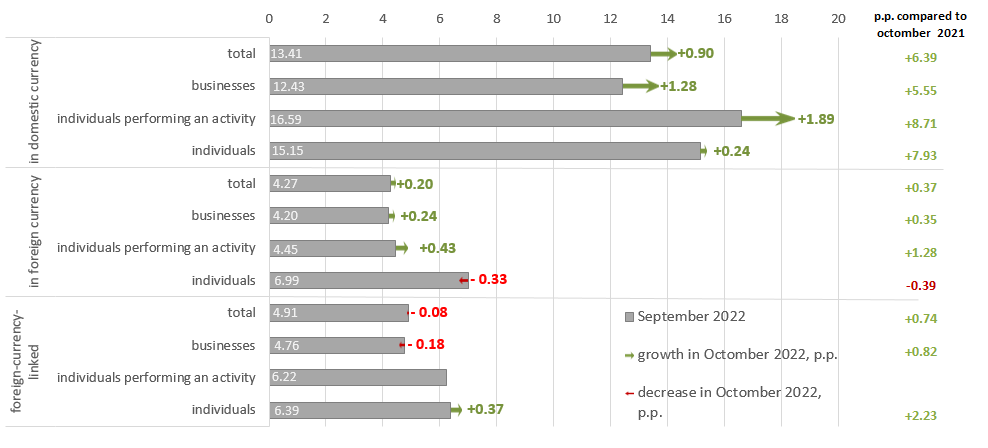

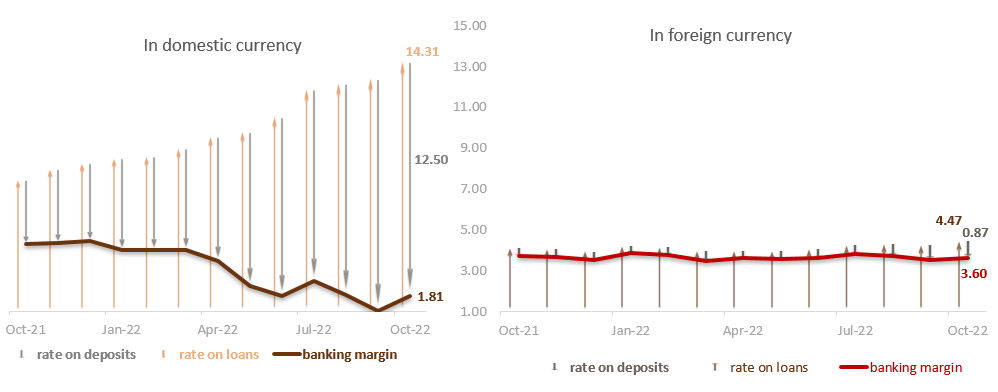

The average nominal interest rate on new loans extended in domestic currency constituted 14.31%, on loans in foreign currency – 4.47%, and on foreign-currency-linked loans – 4.83%.

Compared to the previous month, the average rate evolved as follows (Chart 4):

Compared to the similar period of the previous year, the weighted average nominal interest rate on domestic currency loans increased by 6.39 p.p., on those in foreign currency – by 0.38 p.p., and on foreign-currency-linked loans – by 0.74 p.p.

Chart 4

Weighted average nominal interest rates on new loans, %

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

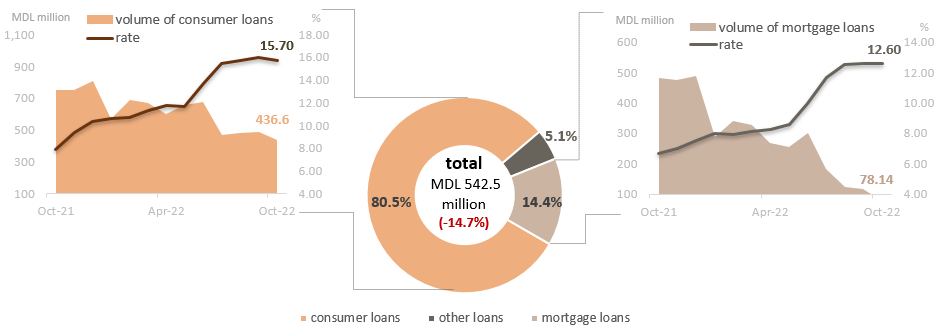

The volume of domestic currency loans extended to individuals decreased in October 2022 by 14.7%, as compared to the previous month, and totaled MDL 542.5 million (Chart 5). The average rate on these loans increased by 0.24 p.p.

Chart 5

Domestic currency loans extended to individuals

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

From the perspective of the purpose of loans extended to individuals, consumer loans held the largest share (80.5%), and were extended at an average rate of 15.70% (-0.28 p.p. compared to the previous month and +7.85 p.p. compared to October 2021).

The average rate on mortgage loans extended in domestic currency decreased by 0.01 p.p. compared to the previous month and by 5.94 p.p. compared to October 2021 and totaled 12.60%.

It should be noted, that 75.9% of total mortgage loans were extended in domestic currency. Consumer loans also were mainly extended in domestic currency (99.9% of total consumer loans).

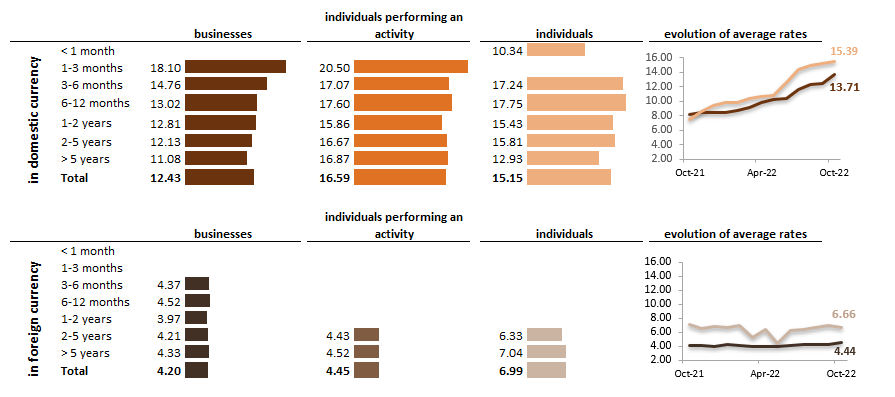

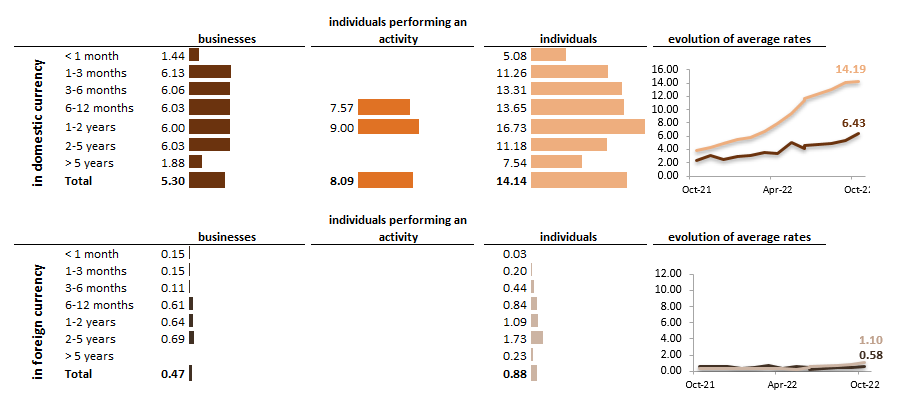

Domestic currency loans (Chart 6) with maturity from 2 to 5 years (MDL 1,040.78 million, recording the highest demand in the reporting month), were extended at an average interest rate of 13.95% (12.59% – on businesses loans, 18.66% – on individuals performing an activity loans, and 15.61% – on individuals’ loans).

Chart 6

Average rates on extended loans, by maturity, %

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

The highest average rate on domestic currency loans was registered on loans with maturity from 1 to 3 months and amounted to 20.43%.

Loans in foreign currency with terms of 2 to 5 years (MDL 1,123.47 million, which had the highest volume in the reporting month) were extended at an average rate of 4.33%, businesses loans – 4.32% (MDL 1,119.48 million), and individuals’ loans – 7.00% (MDL 3.99 million). Individuals performing an activity did not request this type of loans (Chart 6).

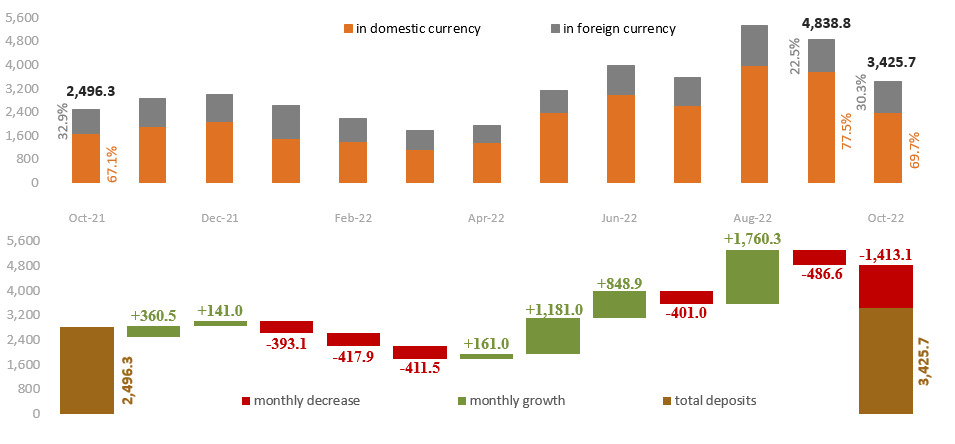

In October 2022, the new term deposits totaled MDL 3,425.7 million, decreasing by 37.2% as compared to October 2021 (Chart 7).

Chart 7

Dynamics of term deposits (upper chart) and change from the previous month (lower chart), million MDL

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

The volume of new term deposits constituted:

The share of deposits attracted in domestic currency constituted 69.7%, of those in foreign currency – 30.3%.

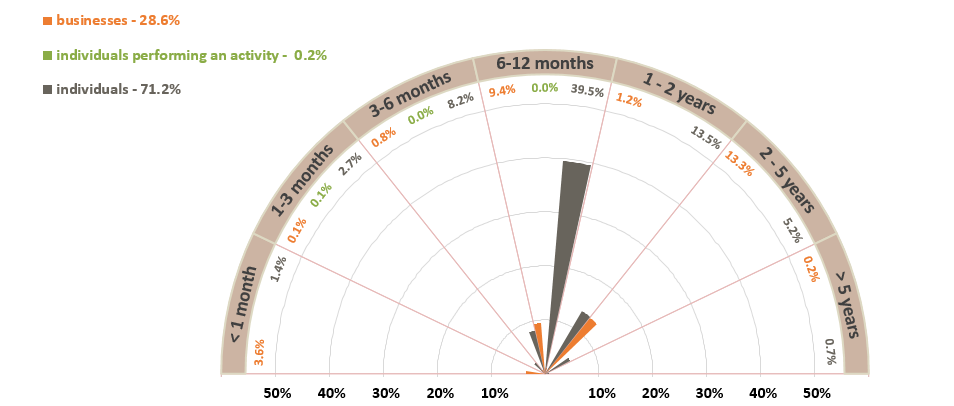

Individuals’ deposits (Chart 8) represented the largest share of total deposits - 71.2% (where 54.5% represents domestic currency deposits and 16.7% – foreign currency deposits).

Chart 8

New term deposits placed by maturity and their structure, %

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

In terms of maturity, the highest demand was recorded for deposits with terms from 6 to 12 months, which held 49.0% of total term deposits (39.5% – individuals’ deposits).

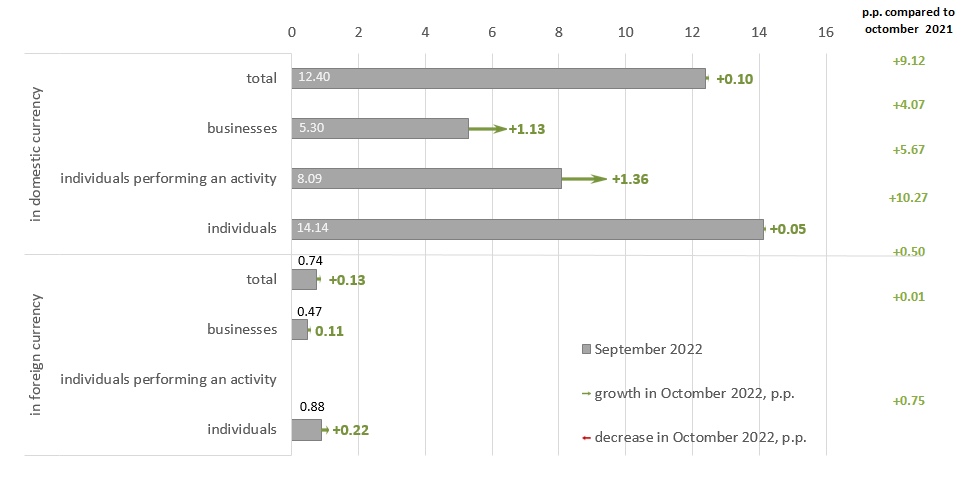

The average interest rate on domestic currency term deposits constituted 12.50%, and on those in foreign currency – 0.87%.

Chart 9

Weighted average rates on new term deposits, %

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

Compared to the previous month, the average rate evolved as follows:

Compared to October 2021, the average interest rate on domestic currency deposits increased by 9.12 p.p., but that on foreign currency deposits – by 0.50 p.p. (Chart 9).

Chart 10

Average interest rates on new term deposits, by maturity, %

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

Domestic currency deposits with maturity from 6 to 12 months, holding the highest share (50.2% of total deposits in domestic currency), were attracted at an average interest rate of 13.14% (businesses’ deposits were attracted at an average rate of 6.38%, while individuals’ deposits – at a rate of 13.98%), %, while individuals performing an activity – at a rate of 8.00%) (Chart 10).

In the case of foreign currency deposits, the largest share (46.3%) is held by those with terms from 6 to 12 months, which were placed at an average interest rate of 0.69% (businesses placed their deposits at a rate of 0.47%, individuals – at a rate of 0.84%).

The highest average rate on domestic currency deposits was recorded as follows:

The highest average rate on foreign currency deposits was recorded as follows:

Chart 11

Bank interest margin, p.p.

Source: NBM report on average rates and volumes of new loans and new deposits attracted for October 2022

The interest rate margin on operations in domestic currency increased by 0.80 p.p. compared to the previous month and decreased by 2.73 p.p. as compared to October 2021 (Chart 11).

The interest margin on foreign currency transactions increased by 0.07 p.p. compared to the previous month and decreased by 0.13 p.p. as compared to October 2021.

Note. Aggregate data may not correspond exactly to the sum of the components due to mathematical rounding.

1. Data presented according to Instruction on preparation and presentation of reports on interest rates applied by banks in the Republic of Moldova, approved by Decision of the Executive Board of the NBM No 331 of 1 December 2016, Official Monitor of the Republic of Moldova No 441-451 of 16 December 2016, as subsequently amended and supplemented.

2. Loans foreign-currency-linked, according to the Regulation on the open currency position of the bank, approved by Decision of the Council of Administration of the National Bank of Moldova No 126 of 28.11.1997, Official Monitor of the Republic of Moldova No 112-114/198 of 14.10.1999, with further modifications and completions, refer to the assets which balance, according to the conditions established in the relevant contracts concluded by the bank, shall be modified depending on the evolution of the exchange rate of Moldovan currency against the attached exchange rate.

3. Individuals performing an activity, in accordance with the Instruction on completion by licensed banks of the Report on monetary statistics, approved by the Decision of the Executive Board of the NBM No 255 of 17 November 2011, Official Monitor of the Republic of Moldova No 206-215 of 2 January 2011, as subsequently amended and supplemented, work in associations without legal personality and are producers of goods and/or services for market, and namely, individual enterprises, farms, entrepreneur license holders, notaries, lawyers, bailiffs, etc.