Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

Published in the Official Monitor of the Republic of Moldova no.223-230/1161 of 08.08.2014

Approved by Decision of the

Council of Administration

of the National Bank of Moldova

No.147 of 31 July 2014

Recommendations

on Identification of Beneficial Ownership

I. General provisions

1. Recommendations on Identification of Beneficial ownership (hereinafter Recommendations) are intended to provide some methodological guidance to banks and other payment service providers in applying the legislation on preventing and combating money laundering and terrorist financing in the process of identification of the beneficial ownership (beneficial ownership) of the legal entity or individual, customer of the bank or other payment service provider. The Recommendations are developed taking into account the legislation on preventing and combating money laundering and terrorist financing.

2. These Recommendations cover:

a) description of the procedure for determining the individual(s) owning at least 25% of shares or voting right of the legal entity;

b) description of the procedure for determining the individual(s) who ultimately controls (control) an individual or legal entity;

c) description of the procedure for determining the individual(s) on whose behalf a transaction is performed or an activity is carried out;

d) description of the procedure for implementing the risk-based approach for the identification of the beneficial ownership.

3. The Recommendations are developed taking into account the 40 Recommendations of the Financial Action Task Force (FATF-GAFI), Wolfsberg Group documents related to identification of beneficial ownership in the context of private banking services, BASEL documents on know-your-customer or other related international documents.

4. Terms and expressions used in these Recommendations have the meanings set out in the Law no.190-XVI of 26.07.2007 on preventing and combating money laundering and terrorist financing, Regulation no.172 of 04.08.2011 on banking activity in preventing and combating money laundering and terrorist financing, as well as recommendations and guidelines related to the field.

5. Compliance with the recommendations on the identification of beneficial ownership will facilitate the identification, evaluation and minimization of risks and vulnerabilities related to the activity of banks and other payment service providers in relation to their customers.

II. Identification and verification of beneficial ownership

6. One of the basic tasks applied in the know-your-customer process is the identification and verification of beneficial ownership of the legal entities and their holding in the share capital. The identification and verification of the beneficial ownership (owners) is essential for taking the right decision on the level of risk of money laundering and terrorist financing associated with the customer. Some legal entities hide intentionally the identification of real owners/beneficial ownership and the persons who control the activity of the legal person. Sometimes, the identification and verification of beneficial ownership of the customers may be difficult because of a complex but legitimate ownership structure, such as the existence of more hierarchical founding companies with more founders and associated members. However, banks and other payment service providers should be alert to the possibilities used to hide or mask the beneficial ownership.

7. These recommendations are applied to bank customers and other payment service providers. Thus, the recommendations provide information for determining the beneficial ownership by identifying the individuals who hold more than 25% of the share capital of a customer exercising effective control on the customer and on whose behalf are made the transactions.

8. Difficulties may be encountered in understanding the concept of “beneficial ownership” used in different context when applying the rules in preventing and combating money laundering and terrorist financing. In this context, the annex to these recommendations highlights and explains the term “beneficial ownership” used in practice.

9. Increased risks may arise in relation with beneficial ownership of accounts, because the nominal account holders may allow individuals and legal entities to hide the true identity of assets or proprieties derived from criminal activities or associated activities. Moreover, the persons performing money laundering and/or terrorist financing, tax evasion, the criminals and terrorists might use the confidential data and information of some companies, including shell companiesShell company - company that conducts fictitious activity (dummy, delinquent, “for a day”, etc.), which aims to cover the unlawful acts of the subjects of entrepreneurship, institution or organizations engaged in legal activities by putting at their disposal bank accounts and documents of strict evidence aimed at the tax evasion, legalization of smuggled and illicit goods, dissimulation of money source and removal of money from the legal circuit of the national economy, theft of the owner wealth and/or other economic and financial and fiscal interests. Criteria for determining shell companies may be found in the CAN Oder no.83 and IFS no.215 of 05.08.2009 for the approval of the Regulation on criteria for identifying companies created with the intention to conduct fictitious entrepreneurial activity. to hide the nature and purpose of illicit transactions and the identity of the persons associated therein. Therefore, the identification of beneficial ownership of some companies can be challenging, because the characteristics of these companies often protect effectively the identity of beneficial ownership. However, a proper identification of beneficial ownership is important for determining properly the suspicious activities and the provision of useful information to law enforcement entities.

10. The bank and other payment service providers may use in their activity various techniques and tests to identify the beneficial ownership of customers. One of the tests that may be applied is determining the existence of the following three elements, taken individually and/or in combination:

a) holding more than 25% of the ownership or voting right, or capital/profit of the customer;

b) having effective control over customer;

c) the person on whose behalf is performed the transaction.

11. If banks or other payment service providers establish business relationship with a customer, they shall identify and verify the identity of the beneficial ownership. Additionally, the ownership structure of the customer shall be established and understand at each level. The beneficial ownership is not necessarily a single individual, there may be more beneficial ownership in the ownership structure. If there is a complex ownership structure with multiple levels and without a reasonable explanation for their existence, banks and other payment service providers shall admit the possibility that this structure was created deliberately in order to hide the beneficial ownership.

12. There may be customers who have no beneficial ownership (state enterprises, municipal enterprises, associations, religious organizations, political parties and other socio-political organizations, foundations, public institutions, central and local government bodies, etc.). In such cases, banks and other payment service providers shall implement appropriate know-your-customer measures, including for determining the purpose and nature of the business relationship and the source of money involved to ensure the non-involvement of banks and other payment service providers in operations of money laundering and/or terrorist financing. In case of suspicions related to their activities, banks and other payment service providers shall inform the Preventing and Combating Money Laundering Service according to the legislation in force.

13. In many cases, the customer shall disclose quickly and clearly information on its ownership structure. In other cases, banks and other service providers shall further inquire into the control or ownership structure and management control, which is more complex. At any phase of this process, it may be decided to stop the completion of this process or it can be found that the information is unobtainable. In such cases, banks and other payment service providers shall decide, based on the normative acts in force related to this field, on the need to refuse to establish a business relationship or shall undertake measures for interrupting the existing business relationship, informing the Preventing and Combating Money Laundering Service according to the legislation in force.

III. Ownership structure

14. It is important that banks and other payment service providers understand the customer’s ownership structure. The possibility that the ownership may be divided into holdings of 25% or less shall be taken into account. However, relations between parties can lead to individual or aggregate ownership, which holding exceeds 25%.

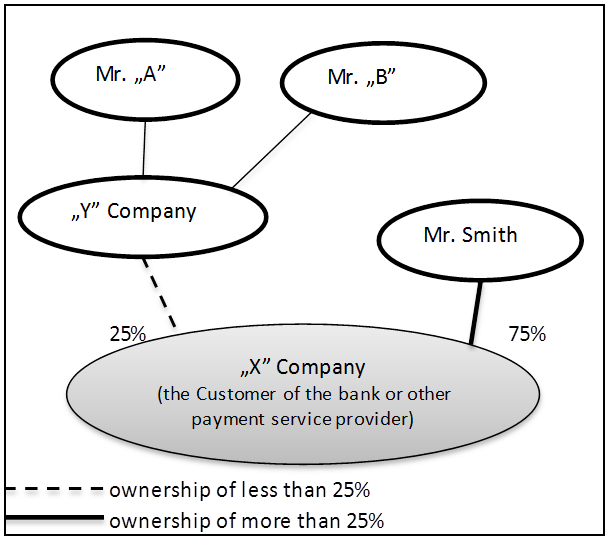

Chart no. 1 – Structure of simple ownership

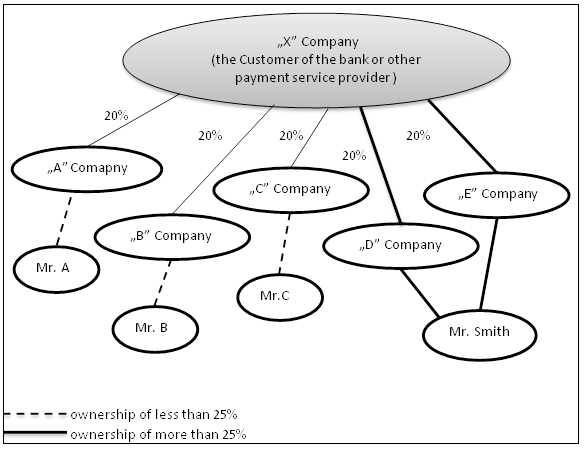

Chart no. 2 – Structure of complex ownership

15. Chart no.1 shows the structure of simple ownership, where the owners of „X” company are Mr. Smith, with a holding of 75% and the company „Y” with the holding of 25%, which is owned by the owners Mr. „A” and Mr. „B” in equal shares. In this way, it appears that the individual Mr. Smith owns 75% of the company’s capital and he is the beneficial ownership of the company „X”, as holding more than 25%.

16. Chart no.2 shows the structure of complex ownership, where the „X” company has 5 owners, each of them holding 20%. Following the information analysis, it appears that the „D” company and „E” company are owned by Mr. Smith. Thus, the individual Mr. Smith owns 40% of the company’s capital and he is the beneficial ownership of „X” company, as holding more than 25%.

17. Using the above-represented test of identifying the beneficial ownership, banks or other payment service providers may determine the identity of the beneficial ownership of the customer. Thus, for some customers, banks or other payment service providers shall undergo one stage when applying this test to determine the individual who is the beneficial ownership, while for other customers, banks or other payment service providers shall undergo more stages when applying this test to determine the individual who is the beneficial ownership.

IV. Effective control (ultimate)

18. For some customers, the application of the test to identify the beneficial ownership will provide banks or other payment service providers the possibility to determine the ownership and, therefore, the beneficial ownership of the customers. However, this test will not provide this opportunity in case of other customers. For example, in case the ownership of a customer – legal entity is divided among a large number of persons, each of them holding less than 25%. This example can be well illustrated in case of production cooperatives, business cooperatives or unlimited liability companies, which have a large number of members and it is unlikely to be a person with a holding higher than 25%. In such cases, banks or other payment service providers shall identify the beneficial ownership applying the technique for determining the effective control over the customer.

19. The effective control over a customer is part of the concept of beneficial ownership. For example, it may be the person who is responsible for the management decisions of the legal entity, or similarly of the customer. Understanding the organizational structure and the activity of the customer will allow banks or other payment service providers to identify the persons who have effective control over the customer.

20. Deciding on the persons controlling effectively the customer - legal entity, banks or other payment service providers shall consider, but without limiting to:

21. The person who has effective control over the customer may be determined by implementing the above-mentioned techniques, which can be applied to the customer. In this regard, banks or other payment service providers shall take into account the management type of the customer and the governing structure, and shall decide who has effective control over the customer.

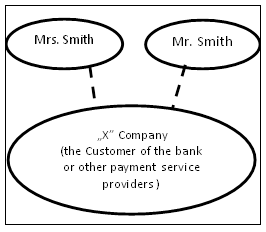

Chart no.3 –Effective control

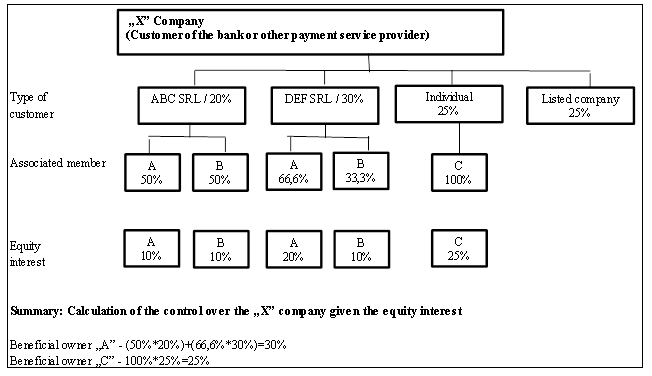

22. Chart no.3 schematically shows the effective control of individuals over the customer. Thus, Mr. Smith holds all voting rights in “X” company. Ms. Smith is responsible for all administrative decisions in „X” company. In this case, it may be considered that both persons fall within the concept of beneficial ownership, as both have effective control. Additionally, Chart no.4 schematically shows the determination of effective control held by an individual over a company with a complex ownership structure.

Chart no.4 – Effective control over a company with a complex ownership structure

V. The person on whose behalf a transaction or an activity is performed

23. Another part of the definition of beneficial ownership is a person on whose behalf a transaction is performed. This concept is important when it is taken into account the relationship between the intermediate person and its customers. There are various scenarios, many of which are complex. However, determining the person on whose behalf a transaction is made, often involves the need to control the intermediate person.

24. Under the legislation in force, banks or other payment service providers shall apply know-your-customer measures. In this regard, a detailed analysis and control of customer’s structure is the main lever to know who is the customer or the person acting on its behalf. There are cases where the person acting on behalf of the customer may be relatively easily identified by confirming the possession of documents that empower the trustee, but there are also situations where the person acting on behalf of the customer may be hardly identified, because there are several intermediate persons who are difficult to be verified and analyzed.

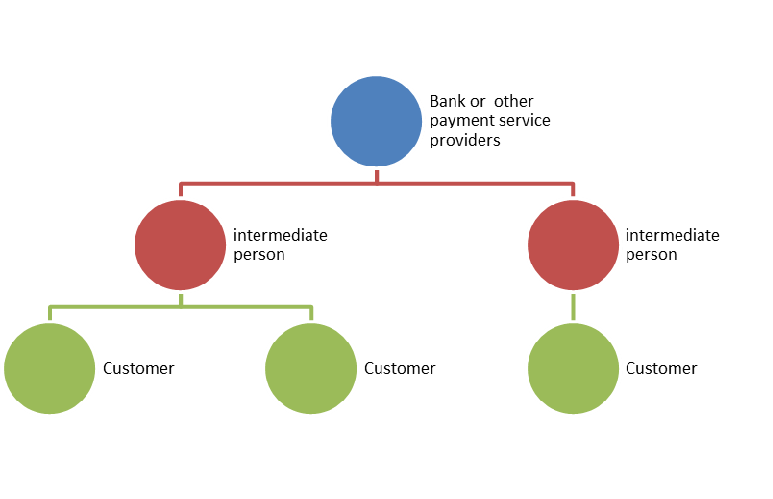

25. The intermediate person may be a financial institution or other legal entity, which has a business relationship or performs transactions with a bank or other payment service providers in relation with the products or services provided for their customers. Chart no.5 illustrates the concept of the intermediate person.

Chart no. 5 –Intermediate person

26. An intermediate person may be itself a reporting entity. At the same time, it may have in turn an intermediate person managing the customer and sometimes there exists a chain of intermediaries/ reporting entities managing the customer. Thus, the person managing the activities of the investment companies and financial consultants are examples of intermediate persons and the investor is the final basic customer.

27. In the context of an investment structure involving one or more intermediate persons, the customer of banks or other payment service providers will be the person benefiting from facilities as a result of a business relationship, or performing an occasional transaction through banks or other payment service providers. In this regard, a conclusive example is when the person managing the activity of the investment company provides investment services to an investor. Thus, these services can be provided directly or indirectly. The person benefiting from the investment services provided by the person managing the activity of the investment company is that on whose behalf the account is opened or the business relationship is concluded. In this case, the customer of banks or other payment service providers may be the investor or the empowered person/trustee, depending on the structure. In such cases, banks or other payment service providers shall be careful when identifying the customer and the person acting on its behalf, in order to avoid false determination thereof.

28. Banks or other payment service providers shall use the concept of beneficial ownership to identify the individuals who are the true beneficial ownership of the customer or intermediate person. In this regard, banks or other payment service providers shall use the following elements: ownership of more than 25% of shares or voting rights, holding the effective control over the customer and the person on whose behalf the transaction is performed. The beneficial ownership is the person that meets either one element or all of them combined.

29. In this context, the customer’s beneficial ownership will be the person that “stands behind” the intermediate person and on whose behalf a transaction is performed. To identify this person, banks or other payment service providers shall use the same elements and described techniques, which means to analyze and verify the information of customer’s ownership structure based on the articles of incorporation and/or extracts provided by the databases on the registration of companies (for example, as database can serve ÎS „CRIS “Register” or other similar databases from abroad).

30. In each case, when analyzing whether a customer is a person on whose behalf the intermediate person is performing transactions, it is necessary to take into account to what extent the relationship between the transactions of the intermediate person and the risks and/or benefits shared by the customer is interconnected.

31. If the main purpose of a transaction performed by an intermediate person is to invest funds on behalf of a customer, even if a predefined profit is taken by it, this customer shall be considered the person on whose behalf a transaction is completed. This is the case when the customer has rights or direct control over the transactions performed by the intermediate person.

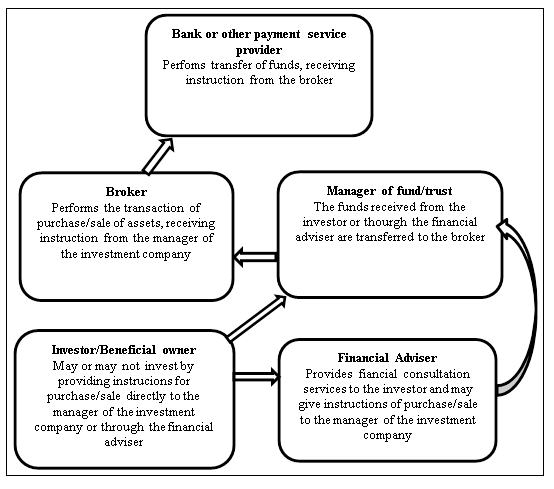

32. If a company issues bonds, shares or other securities to finance its activity (where the main activity purpose of the company is not simply to invest funds obtained from the investors/customers), any transaction made by it shall not be considered as being made on behalf of investors, because there does not exist a connection between the transaction and the risks/benefits associated with them. Chart no.6 shows an classical example of complex structure when the customer of banks or other payment service providers acts on behalf of another person. It should be noted that there are representatives of more intermediate persons between the investor/customer and banks or other payment service providers, providing various services that can be in turn themselves reporting entities.

Chart no.6 – Customer acting on behalf of another person

VI. Risk-based approach

33. To identify the beneficial ownership of a customer is an obligation that shall be fulfilled, irrespective of the degree of risk associated with the customer. However, banks or other payment service providers may vary the approach when deciding on the reasonable steps to be taken to satisfy the correctness of customer information, depending on the customer risk evaluation. The process of customer risk evaluation and the decision on how to identify and verify the beneficiary ownership shall be provided in the internal programs of banks or other payment service providers. This shall be based on the risk evaluation conducted by banks or other payment providers in the field of preventing and combating money laundering and terrorist financing.

34. When there are sufficient reasons for suspicion of money laundering and terrorist financing, banks and other payment service providers shall take know-your-customer measures and to report the transaction to the competent authority according to the legislation in force.

35. The risk-based approach provides flexibility to banks and other payment service providers in using data, documents or other information obtained from a reliable independent source to verify the identity of the beneficial ownership of customer. This shall be applied on a case-by-case basis, by utilizing in particular the following steps:

a) collection of information – at this phase, banks or other payment service providers shall identify the customer/person that aims to perform transactions. Identification measures for understanding the nature and purpose of the business relationship and the ownership structure shall be applied. Banks and other payment service providers shall obtain documents and information related to the business growth level forecast (for example, the business plan). Banks and other payment service providers shall obtain sufficient information, which would give them the possibility to determine whether due diligence measures will be taken or the source of funds will be established.

b) identification of beneficial ownership – at this phase, banks or other payment service providers shall identify the beneficial ownership and the persons authorized to act on behalf of the customer. As customer due diligence measures are required to be applied (standard measures, due diligence measures or simplified measures) may be clearer at this phase, banks or other payment service providers shall require additional documents and additional information related to know-your-customer, depending on the involved degree of risk. Banks or other payment service providers shall apply appropriate measures to verify the provided information.

c) application of risk-based approach to verify the identity of the beneficial ownership – depending on the involved degree of risk, banks or other payment service providers shall verify the information related to the beneficial ownership identity, using the techniques and methods described in the regulations in force.

36. When assessing the risk, banks or other payment service providers shall plan steps according to which different types of customers will be verified. For example, a company intends to become a customer of bank or other payment service providers. At first, banks or other payment service providers shall identify the customer and the beneficial ownership and obtain the standard identity documents related to their know-your-customer measures. The risk evaluation carried out by banks or other payment service providers can determinate the customer classification in the corresponding risk category. Thus, depending on the assigned degree of risk, banks or other payment service providers may decide to verify the beneficial ownership using public information, consulting public databases or websites that contain public information or obtaining confidentially documents and additional information from the customer or other institutions (bodies).

VII. Final provisions

37. Banks or other payment service providers shall organize the internal monitoring system of information about their customers to ensure that the identification and verification of the beneficial ownership in banks or other payment service providers is respected for all customers and is updated accordingly.

38. The proper implementation of know-your-customer measures for the beneficial ownership of customers means adapting the internal policies at new techniques and methods used in the field of preventing and combating money laundering and terrorist financing and using the risk-based approach to verify the beneficial ownership’ identity.

Annex

to the Recommendations on

identification of beneficial ownership

1. What does the „beneficial ownership” mean in the context of a bank account?

The term „beneficial ownership”, when used for determining a beneficiary’s bank account in the context of preventing and combating money laundering and terrorist financing, is conventionally understood as equating to ultimate control over the funds in such account, whether through property ownership or other means. “Control” in this sense is to be distinguished from mere signature authority or legal title.

The term reflects a recognition that a person in whose name an account is opened with a bank is not necessarily the person who ultimately controls such funds. This distinction is important because the focus of efforts in the field of preventing and combating the money laundering and terrorist financing needs to be on the person who has this ultimate level of control. Placing the emphasis on this person is typically a necessary step in determining the source of wealth.

2. What does the term „beneficial ownership” mean in the context of individuals?

When an individual seeks to open an account in his/her own name, banks or other payment service provides shall inquire whether such person is acting on his/her own behalf. If such person responds affirmatively, then, in the ordinary case, it is reasonable to presume that he/she is the beneficial owner.

There are circumstances, however, when this presumption may no longer be reasonable, that is, when “doubt exists” as to whether the apparent account holder is acting on his/her own behalf. In the client acceptance process, for example, such doubt could arise if there are inconsistencies in the information gathered in the due diligence process. For example, if a prospective client’s explanation as to the sources of his/her wealth does not, on its face, make sense, further due diligence would be appropriate.

After the account has been opened, subsequent activity in the account may become inconsistent with the originally anticipated account activity, in which event, it may be reasonable to revisit the initial presumption that the account holder was acting on his/her own behalf. If it is anticipated that the client, after the account is opened, will have occasional transfers of certain predetermined amounts and there are suddenly frequent transfers substantially in excess of that amount, further due diligence may be warranted, including further inquiry as to beneficial ownership.

3. What does the term „beneficial ownership” mean in the context of a legal entity that has a single founder/partner?

If an individual holds assets through a legal entity, then the company is the client and the individual is the beneficial owner of this company. In these circumstances, banks or other payment service providers shall apply due diligence measures to determinate the structure of ownership and control, verify databases and inquire information about the source of wealth of the beneficial owner.

A company with a single founder/partner needs to be approached differently than a corporate entity that has as shareholders many individuals. However, there may be situations where there is more than one beneficial owner. For instance, a successful entrepreneur may organize a private holding company in which he and his spouse are the shareholders/associated members, but in which he is the provider of funds. In this situation, due diligence as to the source of funds and wealth should be done on him, not his spouse. It may, however, be appropriate to engage in some due diligence with respect to the spouse’s reputation and funds.

It is appropriate for the banks or other payment service providers to develop an understanding of the company’s structure. In the event, for example, there are shareholders/associated members owning substantial amount of shares/ interests who are not related to the apparent provider of funds, the banks or other payment service providers should seek to understand why this is so. Similarly, if there are individuals who are in a position to exert control over the funds held by the company (e.g. directors or persons with power to give direction to the directors) and such individuals are not related to the apparent provider of funds, the banks or other payment service providers should consider why this might be so. In these types of situations, this further inquiry may disclose that the apparent provider of funds is not to be viewed as the beneficial owner with respect to such funds. If so, the focus of due diligence should be redirected to the beneficial owner, or indeed, the propriety of opening an account at all may be called into question.

4. What does the term „beneficial ownership” mean in the context of a trust?

In the typical case, it would be clear which person has “beneficial ownership” of such a company. For instance, in the case of an industrialist who establishes a trust for the benefit of his wife or minor children, the “beneficial owner” would be the industrialist settlor, namely, the “provider of funds”. The appropriate due diligence should be conducted with regard to the industrialist, including background checks and the requisite inquiry as to the source of wealth.

Even though the wife and children have a beneficial interest in the trust for trust law purposes (indeed for such purposes they might appropriately be referred to as “beneficial owners”), they should not be treated as “beneficial owners” for AML purposes. That is, it would not make sense to conduct due diligence with respect to the wife’s or children’s source of wealth, although it may be appropriate to do some due diligence with respect to their background and reputation.

This result, incidentally, highlights the consequences of a typical feature of trusts, the separation of legal title and beneficial interest. The person having legal title, i.e. the trustee, typically has control with respect to the assets; however, the parties to the arrangement who have beneficial interests, i.e. the beneficiaries, would typically not have control. The third person, the settlor, as a provider of funds, (who may neither have control, nor a beneficial interest in the assets of the trust) who should, from an AML point of view, be the object of due diligence.

5. What does the term „beneficial ownership” mean in the context of organization without obtaining legal entity status?

Establishing the beneficial ownership in this context generally entails the same principles as those above-mentioned. If such organizations are clients, banks or other payment service providers shall understand the structure of the association and identify who provides the association with its funds and subject such person to appropriate due diligence.