Welcome to the official website of the National Bank of Moldova!

×

Do you have good eyesight and want to turn this tool off?

Welcome to the official website of the National Bank of Moldova!

You can choose one of the most popular reports from the list:

National Bank and the members of its decision-making bodies shall be independent in exercising the tasks conferred upon them by law, and shall neither seek nor take instructions from public authorities or from any other authority.

In order to ensure and maintain price stability over the medium term, the National Bank’s aim will be to keep inflation (measured by Consumer Price Index) at the level of 5.0 percent annually with a possible deviation of ± 1.5 percentage points, considered to be optimal for growth and development of Moldova's economy over the medium-term.

Financial stability is achieved by strengthening the resilience of the financial system, limiting the contagion effect and reducing the accumulation of systemic risks, thus contributing to the sustainability of the financial sector and economic growth.

National Bank shall have the exclusive right to issue on the territory of the Republic of Moldova banknotes and coins as legal tender, as well as commemorative and jubilee banknotes and coins as legal tender and for numismatic purposes.

National Bank is exclusively responsible for the licencing, supervision and regulation of financial institutions activity.

National Bank of Moldova acts as banker and fiscal agent of the State and shall receive from state bodies economic and financial information and documents, which are necessary for carrying out its tasks.

National Bank of Moldova is an autonomous public legal entity and is responsible to the Parliament.

National Bank shall inform the public on the monetary policy strategy on the results of the macroeconomic analysis, the evolution of the financial market and on statistics, including with regard to monetary supply, crediting, balance of payments and the state of the foreign exchange market.

National Bank of Moldova is responsable for the compilation of the balance of payments, international investment position and the statistics of the external debt of the Republic of Moldova.

Inflation Report no.2, May 2014

Although most often used by central banks implementing the inflation targeting regime, measures of core inflation calculated by the method of excluding certain predetermined components, which are determined by external factors, the decisions of authorities or that had a very volatile behavior in the past, have some disadvantages and provide sometimes an incomplete vision on inflationary pressures generated by monetary factors. Thus, these may eliminate some relevant information, and the remaining components may contain transitory information. For example, there is no certainty that the change in prices for some food products, which are generally excluded from the calculation of core inflation, will not contain information on inflationary trends in the economy. Their removal could lead to the elimination of valuable information for decision makers. However, there are factors other than food prices and fuel prices that could compromise the attempts to measure price increases driven by monetary factors, which remain to be included in traditional measures of core inflation.

These deficiencies involve the need for alternative methods of calculation of the core inflation index, based more on statistical techniques and less on the characteristics of the components included in the CPI. Within these measures, the excluded components differ in each period, and their exclusion criterion is determined by certain statistical properties, in this case by how far is the respective component from the central tendency in a certain period and contains no economic substrate. These techniques involve as theoretical guide the monetary concept of inflation compared to the traditional microeconomic concept based on the cost of living.

The method of truncated mean is a statistical method for measuring the central tendency, which is similar to the mean or median. This requires calculating the average after eliminating (trimming) a certain percentage of the two ends of the distribution of price changes. In other words, this means trimming a certain percentage of CPI components that have the highest and lowest prices change in a given period. Typically, the percentage eliminated from the two ends is identical, but there are cases of asymmetric truncated mean. In most cases from 5.0 to 25.0 percent of the ends are truncated.

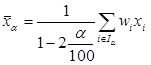

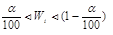

Truncated mean of α - percent is calculated by using the following formula:

, where

, where  is

is

Weighted median represents an extreme case of the truncated mean and represents the growth of the component that is in the middle of the distribution ordered ascending. Thus, half of the monthly increases are under the weighted median and half are above the median. Therefore, the median is calculated according to the previous procedure, but this is the first price increase whose total share is more than or equal to 50 percent.

The annual evolution of the truncated mean (Chart no.1) of inflation is different from the annual growth rate of core inflation calculated by the method of exclusion. Thus, although in early 2010 these recorded similar values, during the year the annual growth rate of inflation measured by the truncated mean recorded a significant growth, which led its trajectory to be superior to the latter, indicating a price increase due to aggregate demand pressures higher than that of the second indicator. In the first quarter of 2011, the truncated mean of inflation experienced a pronounced downward trend, while the core inflation had a relatively stable dynamic. After this episode, by the end of 2011, both indicators recorded an upward dynamic, signaling increasing demand pressures. However, the trajectory of the truncated mean was by about 2.0 percentage points lower. In 2012, both indicators recorded downward trajectories due to slowing economic growth, while the difference between core inflation calculated by the truncated mean method and that calculated by the method of exclusion remained. In 2013, both indicators recorded slight upward trajectories, and at the beginning of 2014 the difference between them is widening.

In early 2010, the weighted median (Chart no.2) had a similar evolution to that of core inflation calculated by the method of exclusion. After a significant reduction in first quarter of 2011, and after a modest increase by the end of the year, the weighted median was significantly lower than the other indicator. Towards the end of 2011, the difference between the two measures of core inflation was about 4.0 percentage points. This difference, however, experienced a decline during 2012 and early 2013 to about 2.5 percentage points. The basic idea of the weighted median is that the pressures from the aggregate demand were significantly lower in the last three years than indicated by core inflation calculated by the method of exclusion.