Bine ați venit pe pagină oficială a Băncii Naționale a Moldovei!

×

Ai vederea bună și dorești să închizi acest instrument?

Bine ați venit pe pagină oficială a Băncii Naționale a Moldovei!

Cele mai populare rapoarte statistice:

Banca Naţională şi membrii organelor de conducere ale acesteia sunt independenţi în exercitarea atribuţiilor stabilite de lege şi nu pot solicita şi nici accepta instrucţiuni de la autorităţile publice sau de la orice altă autoritate.

Banca Naţională informează publicul despre evoluția inflației anuale, strategia de politică monetară,rezultatele analizei macroeconomice, evoluţiei pieţei financiare şi informaţia statistică, inclusiv privind masa monetară, acordarea creditelor, balanţa de plăţi şi situaţia pieţei valutare.

Pentru asigurarea şi menţinerea stabilităţii preţurilor pe termen mediu, Banca Naţională a Moldovei menţine inflaţia (măsurată prin indicele preţurilor de consum) la nivelul de 5.0 la sută anual cu o posibilă abatere de ± 1.5 puncte procentuale, fiind considerat nivelul optim pentru creşterea şi dezvoltarea economică a Republicii Moldova pe termen mediu.

Stabilitatea financiară se realizează prin consolidarea rezilienței sistemului financiar, limitarea efectului de contagiune și diminuarea acumulării de riscuri sistemice, contribuind, astfel, la sustenabilitatea sectorului financiar și creșterea economică.

Banca Naţională a Moldovei, are dreptul exclusiv de a emite pe teritoriul Republicii Moldova bancnote şi monede metalice ca mijloc de plată. BNM pune în circulaţie bancnote şi monede metalice, prin intermediul sistemului bancar.

Banca Naţională este unica instituţie care efectuează licenţierea, supravegherea şi reglementarea activităţii instituţiilor financiare.

Banca Națională supraveghează sistemul de plăţi în Republica Moldova şi promovează funcţionarea stabilă şi eficientă a sistemului automatizat de plăţi interbancare.

Banca Naţională este o persoană juridică publică autonomă şi este responsabilă faţă de Parlament.

BNM publică statistici privind masa monetară, sectorul bancar, balanța de plăți, situația pieței valutare, etc. pentru a asigura transparența în procesul de elaborare și adoptare a deciziilor BNM, a asigura continuitatea în comunicare și predictibilitatea BNM pe piață, pentru sporirea credibilității BNM în calitate de bancă centrală dar și pe piața financiar-bancară din Republica Moldova.

The National Bank of Moldova (NBM) is the designated macroprudential authority, responsible for developing and implementing macroprudential policy in relation to supervised entities. The implementation of macroprudential policy is carried out in accordance with the Macroprudential Policy Strategy (the Strategy), approved in 2023 by the decision of the National Committee on Financial Stability.

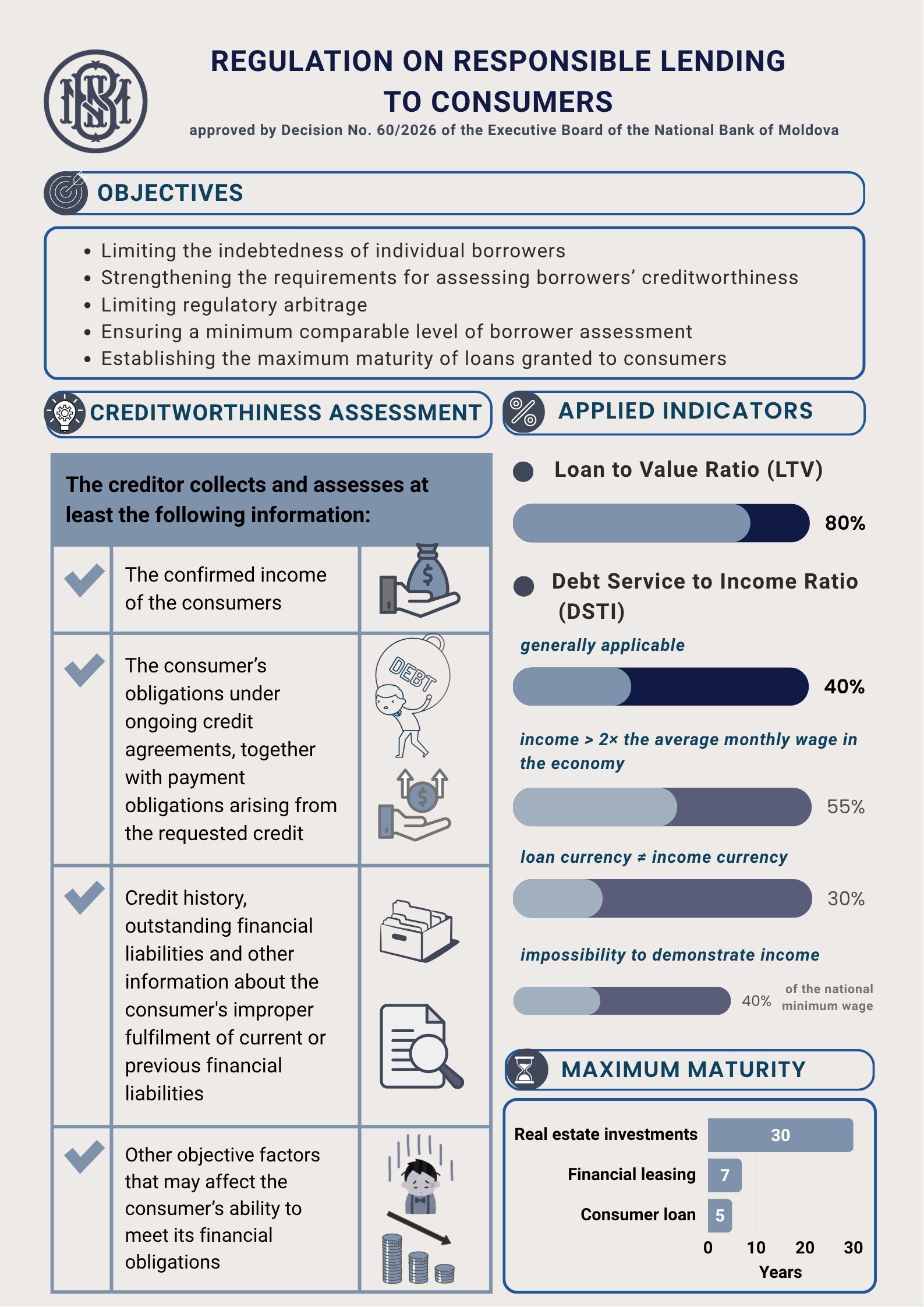

One of the intermediate objectives set out in the Strategy concerns reducing and preventing excessive credit growth and leverage. In this context, to limit the risk of excessive household debt and the significant pressure on repayment capacity, the NBM has established requirements for limiting consumer indebtedness.

Responsible lending requirements

In 2022, responsible lending requirements for consumers were approved both for banks, through NBM Regulation No. 101/2022, and for non-bank credit organizations, through Regulation No. 20/5/2022 of the National Commission for Financial Market

According to these regulations, responsible lending represents the lending activity in which the lender assesses the consumer’s creditworthiness, does not assume a high credit risk, and does not allow the consumer to undertake financial obligations that exceed their financial repayment capacity, thus contributing to the prevention of a rapid accumulation of consumer indebtedness. The assessment of a consumer’s creditworthiness involves analyzing their ability to assume and fulfill the obligations related to a new credit agreement, taking into account their existing credit obligations.

When assessing creditworthiness, the creditor shall ensure the collection and assessment of information, taking into account at least the following:

Limiting certain borrower-level indicators contributes to sustainable lending and, implicitly, to maintaining financial stability while supporting economic growth. In this regard, to ensure responsible borrower eligibility, limits have been established, applicable to both banks and non-bank credit organizations, for the following indicators: the loan-to-value ratio (LTV), the debt service-to-income ratio (DSTI), and the maximum loan maturity.

LTV applies only to loans granted to consumers for real estate investments and cannot exceed 80%, except in cases of refinancing and financing the purchase or construction of another residence, in accordance with the conditions set out in the Regulation. At the same time, if the loan is compensated and/or partially or fully guaranteed by the state, or is partially secured by a real guarantee in the form of deposits, the LTV limit shall be calculated by deducting the value of the loan that is compensated and/or guaranteed.

Example: If a consumer provides a property valued at 1 million lei as collateral, the loan amount granted in this case may not exceed 0.8 million lei, in compliance with the maximum LTV limit of 80%.

DSTI applies to all loans granted to consumers, except for loans granted under the Law on some measures for the implementation of the State Programme “Prima casă”, and must not exceed 40% of the consumer’s confirmed incomes. Thus, the total of the average monthly payments for all of the consumer’s loans at the time the loan is granted, together with the average monthly payment of the requested loan, must not exceed 40% of the consumer’s average net monthly income earned over at least the last six months prior to the submission of the loan application.

Example: If the consumer’s average net monthly income over the last six months is 15,000 lei and he already have other loans with total monthly payments of 2,000 lei, the maximum monthly payment for the new loan may not exceed 4,000 lei, in compliance with the 40% DSTI limit.

Certain exceptions are also provided for, designed to ensure access to financing in justified cases, including for consumers with higher or irregular incomes, without compromising the principles of responsible lending:

At the same time, to limit the accumulation of long-term risks and support sustainable lending evolution, maximum loan maturities have been established for loans granted to consumers: 5 years for consumer loans and 30 years for real estate investment loans. Starting from June 19, 2026, a maximum maturity of 7 years will also be introduced for financial leasing contracts.

Changes to the responsible lending framework, applicable from 2026

Given certain differences between the responsible consumer lending framework applicable to the banking sector and that applicable to the non-banking sector, as well as the need to ensure fair lending conditions, in the context of assuming regulatory and supervisory powers over the non-bank lending sector, the NBM has initiated the process of reviewing and harmonizing responsible lending requirements.

By Decision No. 60 of March 12, 2026 of the Executive Board of the NBM, the Regulation on responsible lending to consumers (Regulation No. 60/2026) was approved, applicable to both banks and non-bank credit organizations. It will enter into force on June 19, 2026.

The revised version of Regulation No. 60/2026 mainly includes the following changes:

- revision and clarification of certain concepts, including “consumer credit”, “real estate investment credit”, “restructured credit”, “price of the mortgaged property”, “market value”, “confirmed income”, “average monthly income”, “debt service”, as well as introduction of the concepts “sensitivity test” and “entrepreneurial, professional or independent activity” (point 6);

- adjustment of the loans categories exempted from the application of the regulation by unifying the list (exemption of loans indicated in Article 2 paragraph (2) letter (h), (i) of Law No. 202/2013) and removing certain types of contracts previously exempted (loans provided in Article 2 paragraph (2) letter (a), (c), (d), (f) of Law No. 202/2013), including loans granted without interest and without other costs (point 3);

- providing further details on provisions regarding the assessment of the consumer’s creditworthiness, including:

- setting a maximum maturity of 7 years for financial leasing contracts (point 45);

- introduction of reporting requirements for non-bank credit organizations to the NBM regarding the values of the LTV and DSTI indicators (point 49);

- clarification of creditors’ responsibility for compliance with the regulation, including loans granted through credit intermediaries (point 50).

The Regulation on responsible lending to consumers aims to prevent excessive consumers indebtedness and to strengthen financial stability, while ensuring fair access to financing.

The requirements set forth apply only to loans and/or financial leasing contracts granted to consumers, that is to natural persons who do not take out the loan for purposes related to entrepreneurial, professional, or independent activities. Therefore, the Regulation does not apply to legal entities or to natural persons who apply for credit for entrepreneurial purposes, provided that such purpose is documented.